When to Incorporate as a Contractor: Beyond $100K

The trades-specific math nobody mentions — WorkSafeBC reclassification, prime contractor liability, and why the limited-liability shield is weaker than you think.

When to incorporate as a tradesperson — the $100K rule, WorkSafeBC reclassification, prime contractor liability, and what limited liability really shields.

Your accountant told you to incorporate when you hit $100K in net income. You hit it last year. You haven't done anything about it. The standard advice gets the threshold roughly right but misses three trades-specific variables that change the math substantially in BC: WorkSafeBC reclassification, the prime contractor liability rule, and the personal-liability shield that's weaker than tradespeople assume.

This post covers when incorporation actually pays off for Canadian tradespeople in 2026 — the real driver (tax deferral on retained earnings), the trades-specific costs nobody mentions, and the structural questions worth answering before you file the articles.

Key takeaways

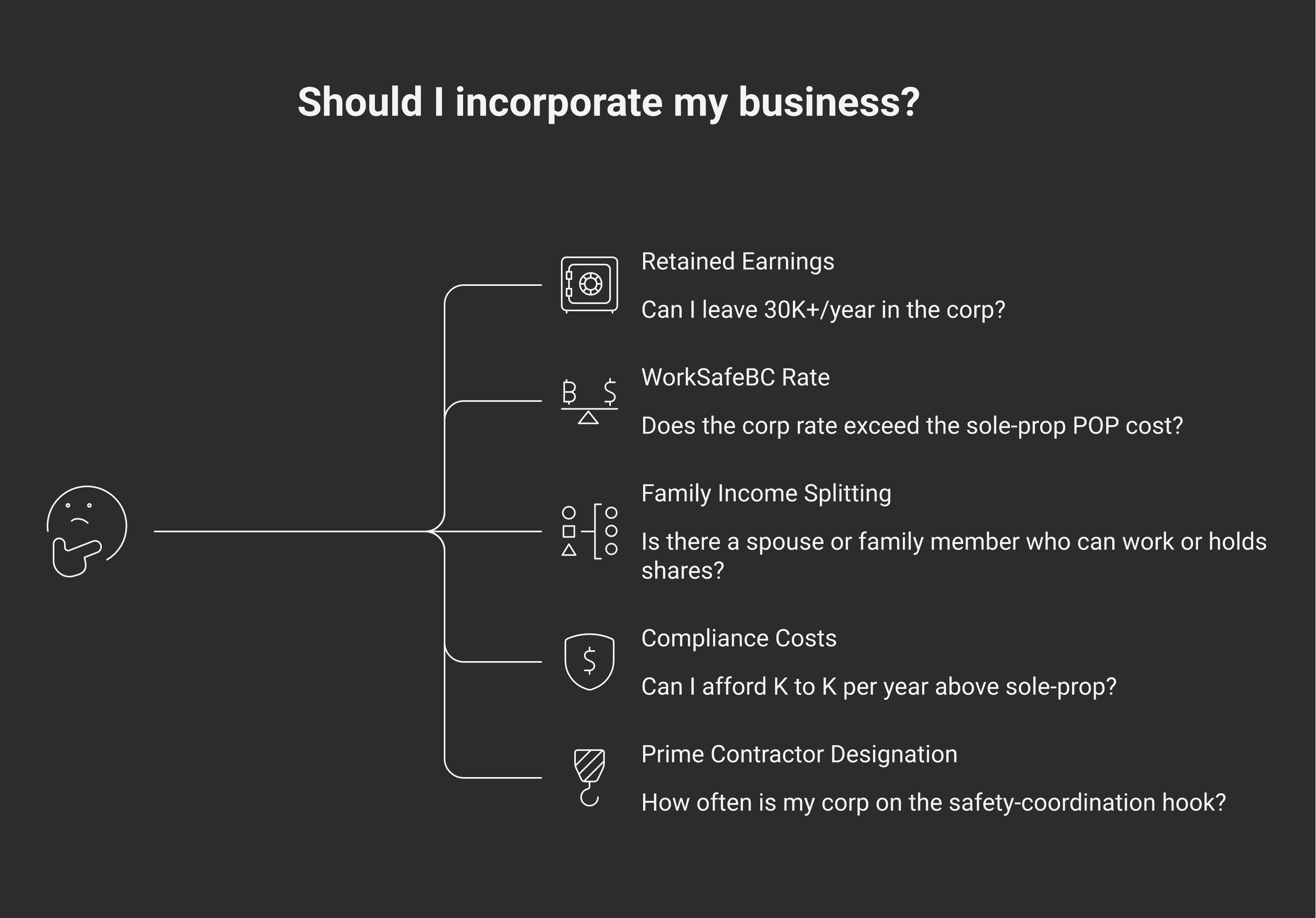

The $100K net-income threshold is a reasonable starting point but not a rule. Real driver: how much income you can leave in the corporation vs. take out personally. If you spend everything you earn, incorporation often doesn't pay.

WorkSafeBC reclassifies you when you incorporate. Most trades go from a "personal optional protection" coverage to a "covered employer" classification — the premium category changes, often substantially. Run the math before you file.

The prime contractor rule under the BC Workers Compensation Act makes the controlling site contractor (typically the GC, but sometimes a substantial sub) responsible for site-safety coordination. An incorporated sub leading a multi-trade portion of work can be designated prime contractor by the GC — bringing new liability you didn't have as a sole prop.

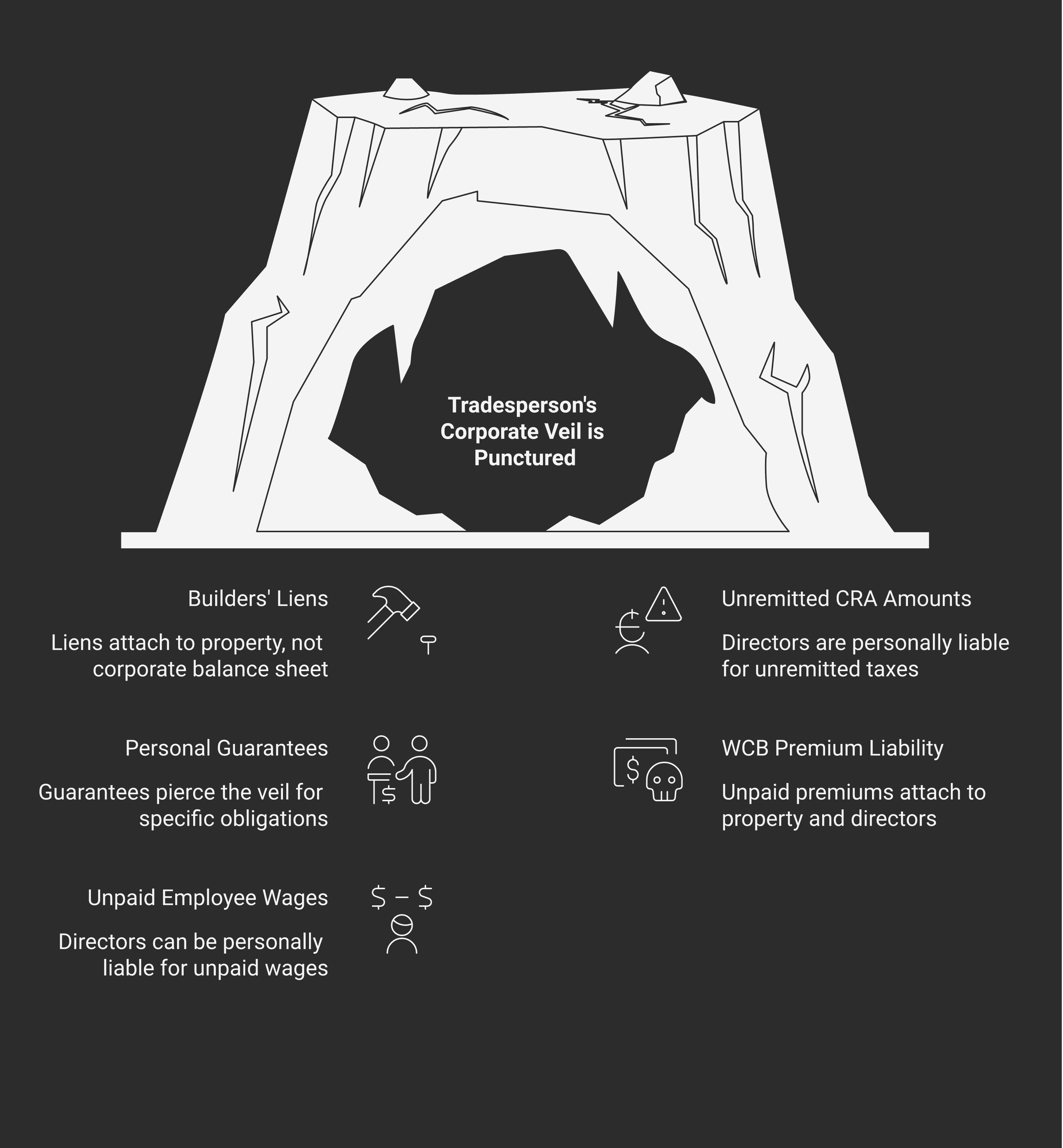

Limited liability is weaker than tradespeople assume. Builders' liens still attach to the property regardless of corporate structure. Directors are personally liable for unremitted GST/HST, source deductions, and certain employee wages. Personal guarantees on bank lines pierce the veil immediately.

The actual reason to incorporate, for most growing trades: tax deferral on retained earnings + family income splitting via dividends. If you can leave $30K-$80K in the corp each year and use the dividend-tax-credit mechanics intelligently, incorporation pays. Otherwise, it's overhead.

The traditional advice and why it's incomplete

The standard advice — "incorporate when you cross $100,000 in net income" — comes from a simple comparison:

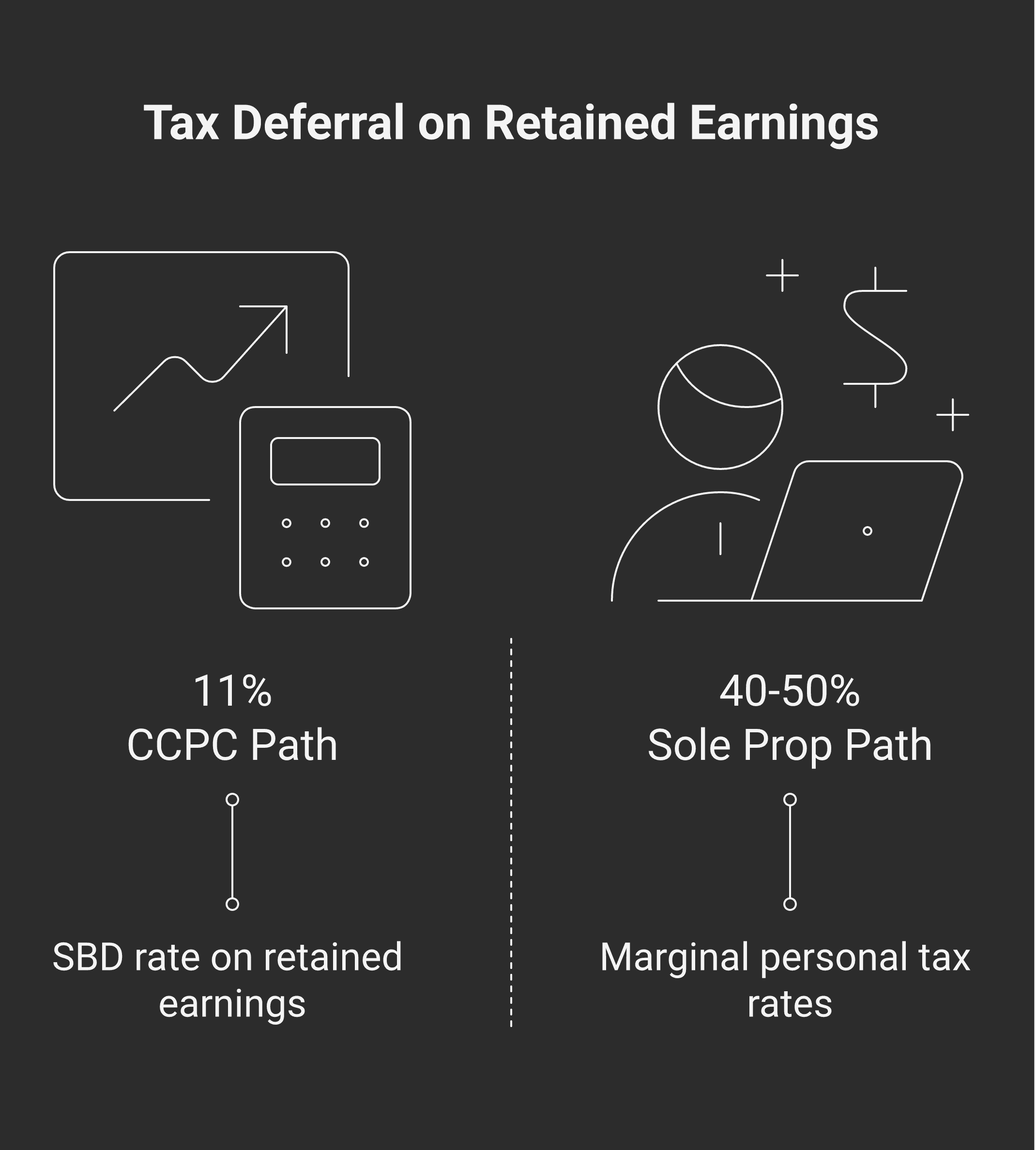

Sole-prop net income above $100K hits the top marginal personal tax brackets (combined federal + BC) in the 40-50% range.

A CCPC paying tax at the small business deduction rate (combined federal + BC) is around 11% on the first $500K of active business income.

The 30+ percentage-point gap is the deferral opportunity if you can leave money in the corp.

That math is correct as far as it goes. What it misses:

The deferral only matters if you actually leave money in the corp. If you draw everything as dividends or salary, you ultimately pay personal tax on it — and integration is designed to make the total tax burden similar to staying a sole prop. You haven't saved tax; you've added compliance.

The costs of incorporation are real: incorporation fees ($300-$1,500 depending on province and use of a lawyer), annual minute-book maintenance, separate tax returns (T2 instead of T1), separate bank accounts and bookkeeping cadence, more complex GST/PST mechanics.

The structural variables — WCB, prime contractor designation, liability shield — change for trades in ways they don't change for, say, software consultants.

Worth reading the Modern Axis "Should You Incorporate Your Business" deep version alongside this post — it covers the universal tax math; this post covers the trades-specific layer.

The real reason: deferral on retained earnings

The single best reason for a trade business to incorporate, in 2026, is tax deferral on retained earnings. If your trade business generates $150K of net income and you only need $80K to live on, the remaining $70K can be left in the corporation, taxed at the small business deduction rate (~11% in BC), and the remaining ~$62K invested by the corp.

In a sole prop, that same $70K of "extra" income would be taxed at your marginal personal rate (call it 40%), leaving you ~$42K. Difference: $20K per year of additional capital that can compound.

That deferral has limits:

Passive investment income earned by the corp reduces the SBD on a sliding scale — the rules under Income Tax Act subsection 125(5.1) start grinding the SBD when passive income exceeds $50K per year. The Modern Axis Small Business Deduction post covers this rule in detail.

Eventually you take the money out. When you do, you pay personal tax on the dividend (with the dividend tax credit reducing the bite). Integration is designed to make the combined tax similar to having paid full personal tax in the year earned — but the deferral itself — the years of compounding at the low corporate rate — is real economic value.

The deferral is most valuable for trades that plan to keep capital in the business — vehicles, equipment, working capital for materials, eventual expansion. Less valuable for trades that pay everything out as it's earned.

If retained earnings aren't on your horizon, the deferral argument doesn't apply, and incorporation needs to justify itself on other grounds.

Family income splitting via dividends

The second material benefit: paying dividends to a spouse or adult family member who holds shares in the corporation, using the dividend tax credit to extract income at lower combined household rates.

The mechanic was reshaped by the Tax on Split Income (TOSI) rules in 2018. TOSI now applies to most dividend income paid to family members who don't meet specific exclusions (working full-time in the business, over 65, or holding shares meeting specific tests). For most trade businesses with a spouse who isn't actively involved in the trade, TOSI applies and the dividend gets taxed at the recipient's highest marginal rate — eliminating the splitting benefit.

But: there are still cases where splitting works. A spouse who works in the business in a genuine capacity (bookkeeping, administration, project coordination — documented hours, market-rate compensation) can be paid wages. A spouse over 65 has a TOSI exemption. An adult child working full-time in the trade business has a TOSI exemption.

A Modern Axis CPA on the personal income tax side can map your specific family situation against TOSI before you set up the share structure. Getting this wrong locks in a structure that doesn't deliver the income splitting you incorporated for.

WorkSafeBC reclassification

This is the variable nobody mentions before you incorporate.

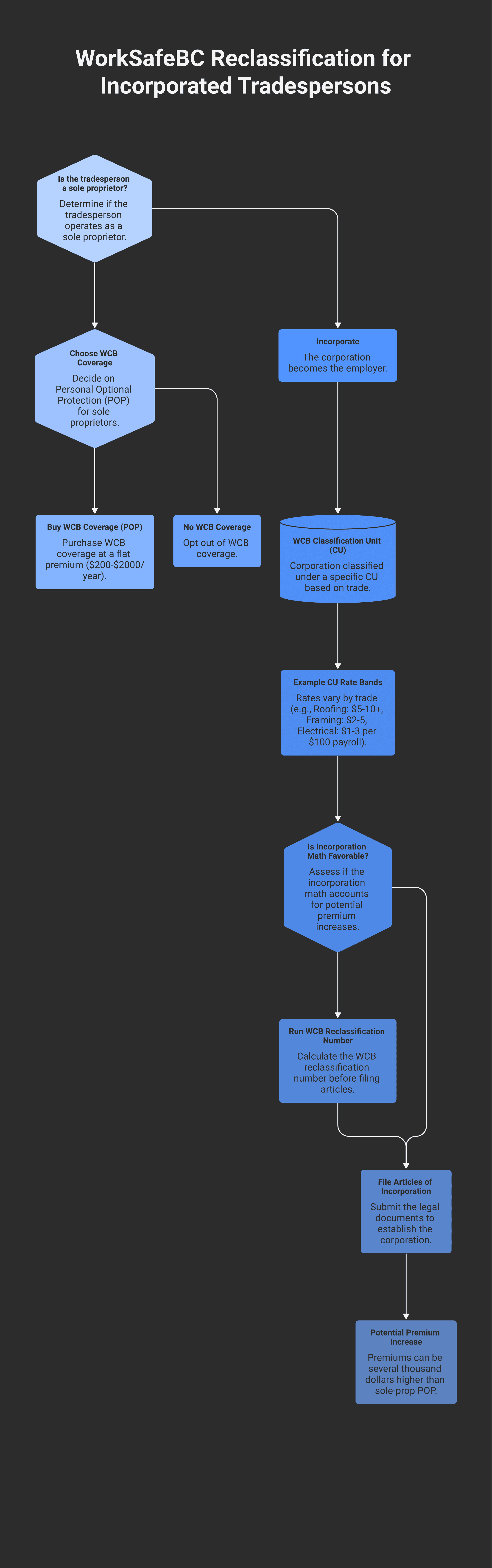

As a sole proprietor in a covered industry, you have one of two coverage modes with WorkSafeBC:

Personal Optional Protection (POP) — sole props who buy WCB coverage on themselves at a flat premium. Most trades opt into this.

No coverage — sole props who don't buy POP. Cheaper but no benefits if injured on a covered worksite.

When you incorporate and start drawing salary from the corporation, you become an employee of the corporation. The corporation is the employer; WCB classifies the corporation under a specific Classification Unit (CU) based on the trade. Your premium rate becomes the CU rate for your specific work — which can be substantially different from your sole-prop POP rate.

Examples of how the CU shift hits:

Roofing CUs have high premium rates (often $5-$10+ per $100 of payroll) because of injury frequency.

Most carpentry / general construction CUs are mid-range ($2-$5 per $100 of payroll).

Specialty trades (electrical, plumbing, HVAC) are lower (often $1-$3 per $100 of payroll).

If your sole-prop POP was $1,500/year and your incorporated CU rate produces a $4,500/year premium on the same income, the WCB cost difference is $3,000 — every year. That changes the incorporation math materially.

Run the WorkSafeBC reclassification math before you incorporate. Your bookkeeper or Contractor Tax Hub can pull your likely CU and premium estimate from the WorkSafeBC published rate tables.

The prime contractor rule

Under the BC Workers Compensation Act and the Occupational Health and Safety Regulation, a "prime contractor" must be designated at every multi-employer worksite. The prime contractor coordinates safety across all employers on site, maintains the site's OH&S program, and bears regulatory responsibility for safety violations.

When a GC contracts your incorporated business for a substantial portion of work — drywall package, framing package, mechanical install — they may designate your corporation as prime contractor for that scope of work. This is a meaningful liability transfer:

Your corp becomes responsible for site-safety coordination among sub-subs (if you bring helpers or sub the work)

Your corp is the entity that absorbs WCB safety-violation penalties

Your corp's directors (you) can face personal exposure under the OHS Regulation for serious violations

This rule didn't exist for you as a sole prop in the same way (a sole prop can be designated prime contractor but it's less common and the corporate-vs-individual structure changes the regulatory frame). Worth understanding before you incorporate if you do work that involves coordinating other workers on-site.

The personal liability shield — weaker than you think

Tradespeople often cite "limited liability" as a reason to incorporate. The shield exists, but trades have specific carve-outs that puncture it:

Builders' liens. Under the BC Builders Lien Act, liens attach to the property being worked on, not to the contractor's corporate balance sheet. If you do unpaid work, your lien runs against the property regardless of whether you're a corp or a sole prop. Likewise, if a sub-sub of yours places a lien on the property, the GC and the property owner deal with it — your corporate veil doesn't change that mechanic.

Directors' liability for unremitted CRA amounts. Under Income Tax Act section 227.1 and equivalent provisions for GST/HST, directors are personally liable for unremitted source deductions and unremitted GST/HST that the corporation owed. If your corp doesn't remit the $30K of source deductions it owed and goes insolvent, the CRA can pursue you personally for that amount.

Personal guarantees on bank lines. Most commercial banks require directors to personally guarantee small-business credit lines and equipment loans. The guarantee pierces the veil for those specific obligations.

WCB premium liability. Under WCB rules, unpaid premiums become an attachment against the property and against the directors personally in certain circumstances.

Employee wages (specific cases). Under BC employment standards rules, directors can be personally liable for up to two months of unpaid wages.

The shield protects against general business torts — a customer suing for breach of contract, a competitor suing for some commercial dispute, a property damage claim from a third party. For most working tradespeople, that's a smaller universe of risk than the carve-outs above. The shield is real but not as broad as "incorporation protects me personally" implies.

The actual decision matrix

Combine the variables and you get a more useful test than "incorporate at $100K":

Consider incorporating if all of these are true:

Net income is above $100K and you can leave $30K+ per year in the corporation

You have specific tax-deferral goals (capital accumulation, eventual sale of the business, retirement compounding)

A spouse or family member can genuinely work in the business (TOSI-exempt) or you have other planning levers

Your WorkSafeBC CU rate isn't dramatically higher than your sole-prop POP rate

You're not constantly designated prime contractor on multi-employer sites (or you've structured for that exposure)

You're comfortable with the ongoing compliance cost (separate T2, minute book, bookkeeping cadence)

Probably stay a sole prop if:

You spend everything you earn (no retained earnings to defer)

Your trade is high-WCB-rate (roofing, certain demolition) and the CU shift wipes out the tax savings

You're a true one-person operation with no spouse/family integration potential

You're new to the trade and your income is still volatile year-over-year

Modern Axis CPA does the structural analysis for trade businesses considering incorporation — running the math on retained-earnings deferral, WorkSafeBC reclassification cost, TOSI applicability, and the holdco-or-no-holdco question. The Modern Axis Holding Companies post covers the next-layer question (when to add a holdco on top of an operating company) if your structure is heading there.

When the incorporation decision lands on Contractor Tax Hub

Contractor Tax Hub supports the structural decision (sole prop vs incorporated, what the right share structure looks like for family planning) at the bookkeeping-side level. The strategic decision belongs to a CPA running the trades-specific math, which Modern Axis covers. Once incorporation is in place, the Premium package handles the ongoing corporate bookkeeping, payroll for the owner-manager, and the GST/HST/PST mechanics specific to incorporated trades.

Frequently asked questions

When should I incorporate as a tradesperson?

The traditional $100K net-income threshold is a starting point, not a rule. The real driver is how much you can leave in the corporation each year — if you spend everything you earn, the tax-deferral benefit doesn't apply and incorporation adds compliance cost without saving tax. Consider incorporation when net income is above $100K AND you can leave $30K+ per year in the corp AND your WorkSafeBC CU shift doesn't wipe out the savings.

What's the actual tax benefit of incorporating?

Tax deferral on retained earnings. A BC CCPC pays roughly 11% combined federal + provincial tax on the first $500,000 of active business income (the small business deduction rate). A sole-prop earning the same income at the top of the brackets pays 40-50%. The 30+ percentage-point gap is the deferral opportunity — but only if you actually leave money in the corp rather than drawing it all out.

How does WorkSafeBC change when I incorporate?

You go from a sole-prop coverage mode (typically Personal Optional Protection at a flat premium) to a covered-employer classification based on the corporation's specific Classification Unit. The premium rate changes — sometimes dramatically. Roofing CUs run $5-$10+ per $100 of payroll; carpentry mid-range; specialty trades lower. Run the math before incorporating; the WCB shift can materially affect the incorporation decision.

What's the prime contractor rule?

Under the BC Workers Compensation Act, a "prime contractor" must be designated at every multi-employer worksite to coordinate safety. When a GC designates your incorporated business as prime contractor for a scope of work (drywall package, framing package), your corp absorbs the regulatory responsibility for safety coordination within that scope — and the directors (you) can face personal exposure under the OHS Regulation. Worth understanding before incorporation.

Does incorporating protect me from being sued?

Partially. The corporate veil protects against general business torts (customer breach-of-contract claims, third-party property damage in many cases). It doesn't protect against builders' liens (those attach to the property), directors' liability for unremitted CRA amounts (source deductions and GST/HST), personal guarantees on bank lines, WCB premium liability in certain cases, or up to two months of unpaid employee wages. Real shield, narrower than tradespeople usually think.

Can my spouse help me save tax through the corporation?

It depends on Tax on Split Income (TOSI). TOSI applies to most dividend income paid to family members who don't meet specific exclusions. A spouse who genuinely works in the business at market-rate compensation (documented hours, real role) can be paid wages — which avoids TOSI. A spouse who doesn't work in the business and just holds shares gets caught by TOSI in most cases. A CPA familiar with TOSI should map your specific family situation before you set up the share structure.

What does it cost to maintain an incorporated business per year?

For a typical small-trade incorporation: $200-$500 in annual minute-book maintenance (your lawyer or a corporate-services provider), $2,000-$5,000/year for a CPA to file the T2 corporate return and provide annual planning, plus the higher monthly bookkeeping cost (incorporated bookkeeping is more involved than sole-prop). Total ongoing: typically $5,000-$10,000/year above what a sole prop would pay. That's the threshold the tax savings have to clear before incorporation pays.

Should I use a holding company on top of my operating company?

For most working tradespeople in the first 5-10 years of incorporation, no — a single operating CCPC handles the trade business and the holdco adds compliance without enough benefit yet. As retained earnings accumulate, as you consider buying real estate for the business, as you approach business sale or succession, a holdco starts to make sense. The Modern Axis Holding Companies post covers when the holdco-on-top structure pays off. It's typically a year 5+ question, not a year 1 question.

Whether to incorporate, when to incorporate, and how to structure your trade business are decisions that depend on more than what's in this post — your net income, your liability exposure, your WorkSafeBC classification, your family situation, and your long-term plans all matter. Treat this as a starting point and talk to a CPA before making the call.