The Personal Services Business Trap for Contractors

The four-factor test, the SBD-denial hit, and the patterns that consistently move an incorporated sub from "employee" toward "real contractor."

Personal Services Business rules for incorporated Canadian tradespeople — the four-factor test, the SBD-denial hit, and how to stay out of the trap.

You incorporated last year. You invoice one general contractor for 85% of your work. They tell you what to build, when to show up, and where to be. You use some of your own hand tools but the GC's tablesaw and scaffolding live on the site. You get paid your hourly rate whether the job runs over or under.

The CRA's view: you're an incorporated employee. Your corporation is a Personal Services Business. Your small business deduction just disappeared. Most of your operating deductions just disappeared. The general corporate tax rate just hit your books — and the CRA can reassess back several years.

This post covers the PSB trap as it actually works for incorporated Canadian tradespeople: the statutory test, the four factors the CRA weighs, what happens to your tax bill when PSB applies, and how to structure the work so you stay out.

Key takeaways

A Personal Services Business is defined in Income Tax Act subsection 125(7) as a corporation that, but for the existence of the corporation, would be reasonably regarded as performing employment-style work for the payor.

PSB classification denies the corporation the small business deduction (SBD) and forces taxation at the general corporate rate (15% federal + provincial general rate, vs the ~9% federal SBD rate). For a BC CCPC, the difference is roughly 11 percentage points of tax on every dollar of PSB income.

Almost all operating expenses are denied when PSB applies. Only salary and benefits paid to the incorporated employee, plus a narrow list of specific deductions, are allowable.

The CRA's test weighs four factors from the common-law employee-vs-contractor analysis: control, ownership of tools, chance of profit and risk of loss, integration. No single factor is decisive; the whole picture decides.

The trap closes when an incorporated tradesperson works for one client for 80%+ of their time and the relationship would look like employment if not for the corporation in the middle. Restructuring the work — multiple clients, own tools, project-based pricing with risk transfer — is the practical defence.

The rule, in one sentence

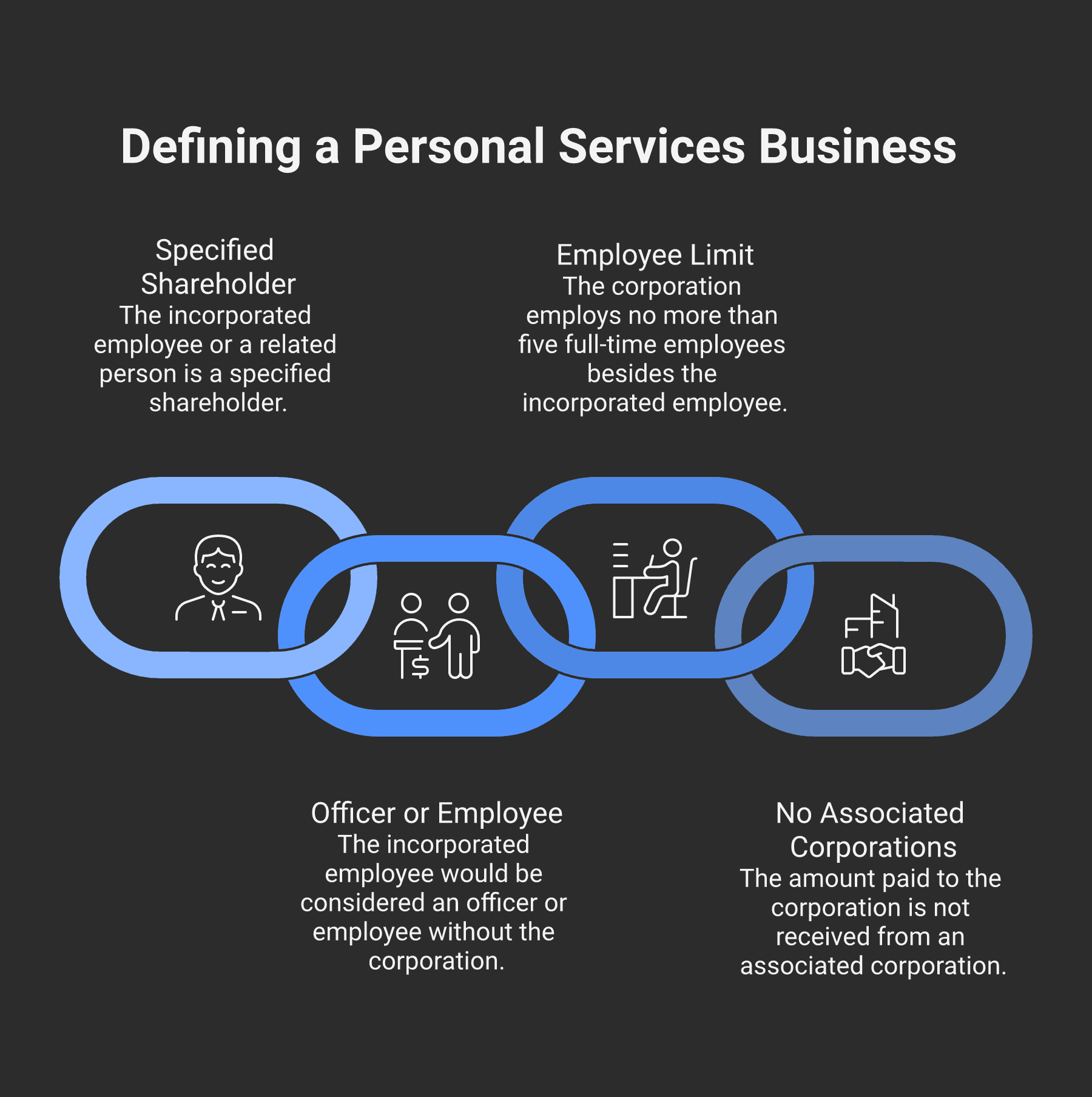

Under Income Tax Act subsection 125(7), a Personal Services Business is a business of providing services where:

An individual who performs the services (an incorporated employee) or a person related to that individual is a specified shareholder of the corporation, AND

The incorporated employee would reasonably be regarded as an officer or employee of the payor (the GC, the property developer, the company hiring the work) if not for the existence of the corporation, AND

The corporation does not employ throughout the year more than five full-time employees other than the incorporated employee, AND

The amount paid to the corporation is not received from an associated corporation.

In trades, conditions 1, 3, and 4 are almost always satisfied automatically (you're the owner, you don't have five+ employees, the payor isn't your associated corp). The fight is over condition 2: would the relationship look like employment if the corporation wasn't there?

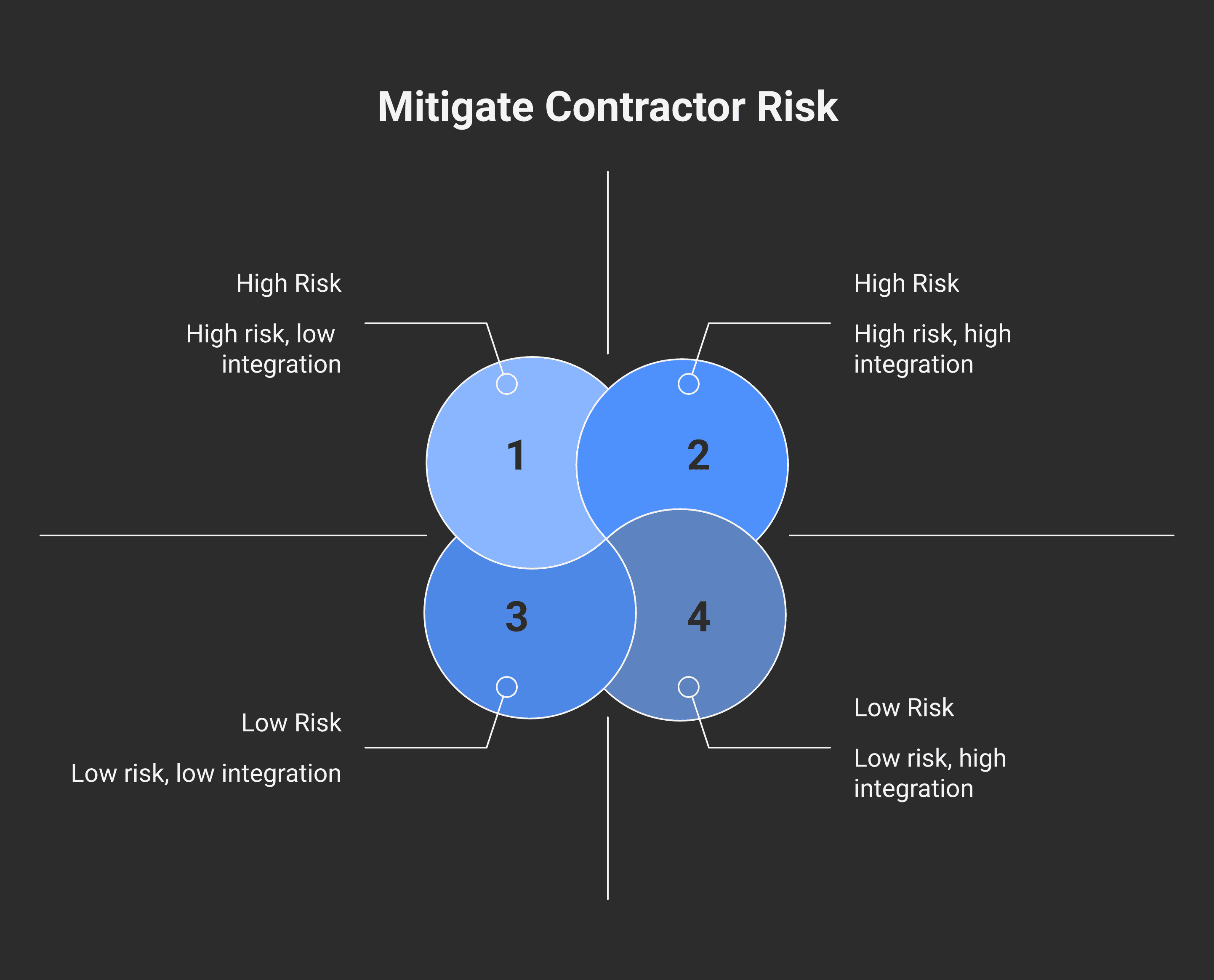

The four-factor test

The CRA's PSB analysis follows the common-law employee-vs-independent-contractor test that runs through every case from Wiebe Door v MNR (1986 FCA) through 671122 Ontario Ltd. v Sagaz Industries (2001 SCC). Four factors get weighed:

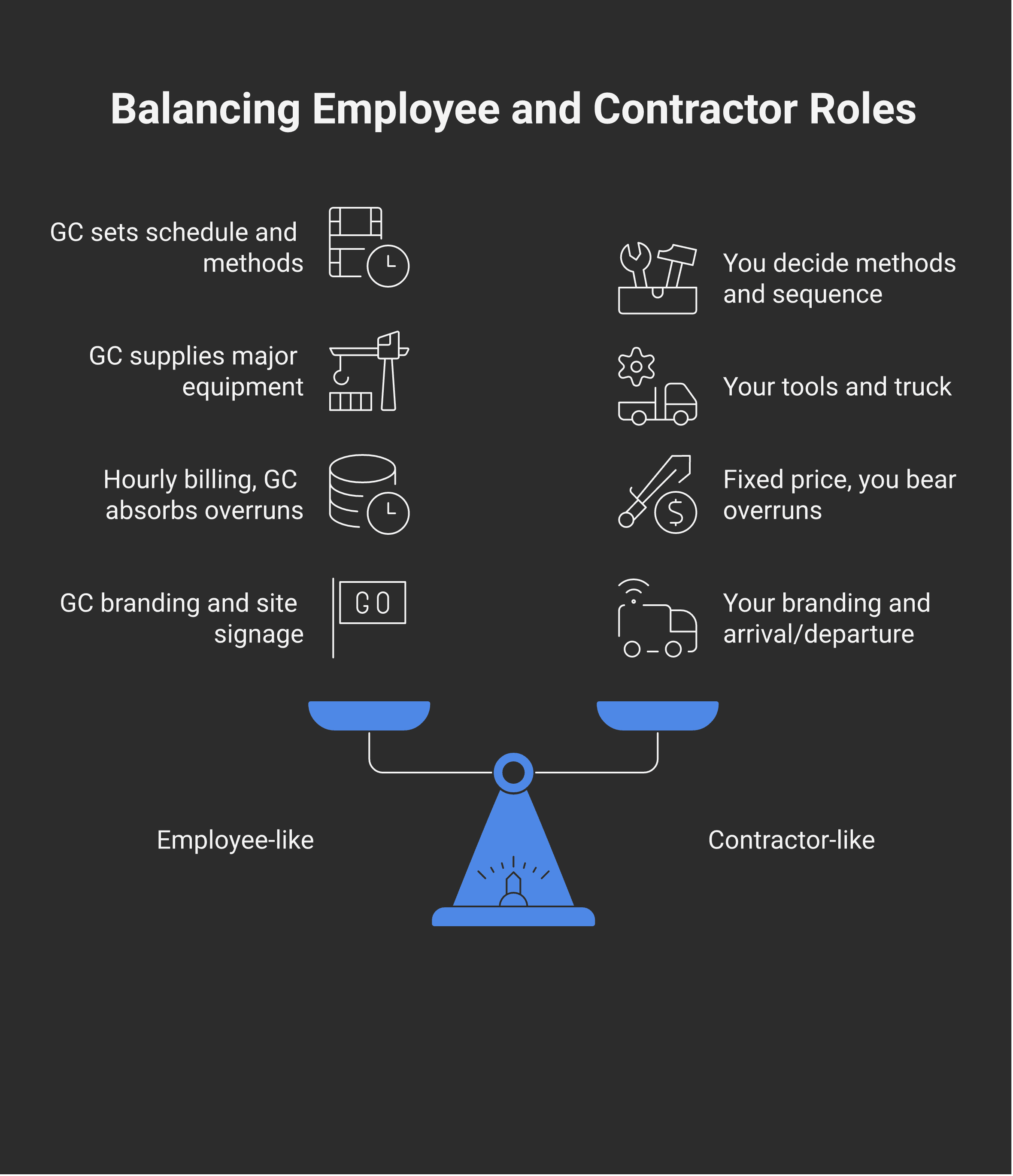

1. Control

Who directs the work? Who decides when, where, and how the work happens?

Employee-like: the GC tells you what to do, when to show up, in what order to build, which methods to use, which materials to install. They set your hours.

Independent-contractor-like: you decide the methods, the sequence, and the hours. You're given an outcome (build this deck to this drawing by this date) and you control the execution.

In trades, control is the easiest factor to lose. A general contractor running a tight schedule will often direct subs minute-by-minute. The more direction, the more this factor leans toward employment.

2. Ownership of tools

Whose tools? Whose vehicle? Whose materials?

Employee-like: the GC's tablesaw, the GC's scaffolding, the GC's materials, the GC's truck.

Independent-contractor-like: your tools, your vehicle, you supply or organize the materials (or you charge for both labour and materials in the contract).

A working tradesperson typically owns a substantial tool kit. This factor often favours the sub — but not always, particularly for finishing trades or specialty work where the GC supplies major equipment.

3. Chance of profit and risk of loss

Do you bear financial risk on the work? Can your profit go up or down based on how you execute?

Employee-like: you bill an hourly rate or a salary. You get paid for time, regardless of project outcome. The GC absorbs cost overruns; you don't.

Independent-contractor-like: you quote a fixed price for the work. If the job takes longer than expected, you eat the cost. If you finish faster, you keep the surplus. You carry liability insurance. You decide which materials at what cost.

This is the factor that bites trades hardest. An hourly-rate sub working under the GC's supervision looks exactly like an hourly-rate employee. Fixed-price contracts shift this dramatically.

4. Integration

Is the sub part of the payor's organization? Is the service essential to the payor's day-to-day operation in a way that's indistinguishable from staff?

Employee-like: you wear the GC's branded vest, drive a GC-marked truck, attend the GC's morning meetings, your name is on the GC's site signage.

Independent-contractor-like: you arrive, do the work, and leave. You wear your own branding (or none). You're not part of the GC's organizational chart.

Integration is subtle in trades — most subs are visibly distinct (their own truck, their own hi-vis) but operationally integrated (they show up at the GC's site, work the GC's schedule). The closer you look like staff, the worse this factor gets.

What happens to your tax bill when PSB applies

Two compounding hits:

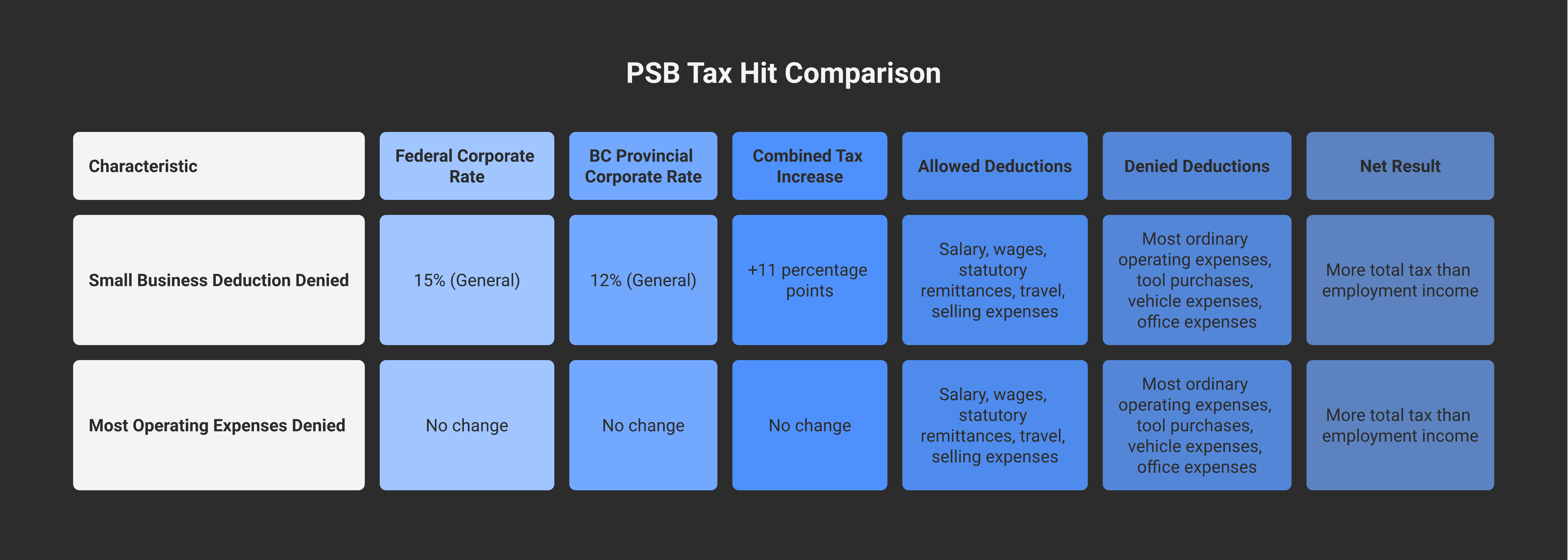

Hit 1: No small business deduction

The PSB-classified corporation cannot claim the small business deduction. Federal tax rate goes from ~9% (SBD) to 15% (general). Provincial goes from BC's ~2% (SBD-eligible) to 12% (general). Combined: roughly 11 percentage points more tax on every dollar of PSB-classified income. (Modern Axis covers the SBD rules and why they matter in detail.)

Hit 2: Most expenses denied

Income Tax Act paragraph 18(1)(p) lists what a PSB can still deduct:

Salary, wages, and other remuneration paid to the incorporated employee

The employer's portion of CPP, EI, and other statutory remittances on that salary

Certain travel expenses required to perform the services

Expenses related to selling the services

A few other narrow categories

What's denied:

Most ordinary operating expenses

Tool purchases and depreciation

Vehicle expenses beyond strict employee-style limits

Office expenses, supplies, professional fees, training

Almost everything you'd normally deduct as an active small business

The combined effect: a PSB-classified corporation pays general-rate tax on near-gross revenue. The shareholder also pays personal tax on the salary they drew. The combined burden frequently exceeds what the same income would have attracted as employment income — making the corporation worse than useless for tax purposes.

The CRA can reassess back several years. Most assessments cover the most recent three normal-reassessment-period years, sometimes more if gross negligence applies.

Staying out of the trap

There's no checklist that guarantees you stay out of PSB classification. The CRA looks at the whole picture. But the patterns that consistently move the analysis toward "real contractor" status:

Multiple genuine clients. Working for one GC at 80%+ of your time is the single biggest risk factor. Working for 3-4 GCs across the year, with no single one dominating, dramatically shifts the analysis. (Modern Axis on the "Should You Incorporate" decision covers the broader structural questions that feed into this.)

Own tools and equipment. Bring your own truck, your own power tools, your own materials when possible. Avoid letting the GC's gear become your default kit.

Fixed-price contracts where possible. Even partial fixed-price (e.g., $X for the framing of this house, plus separate change orders) shifts risk. Pure hourly billing is the riskiest model.

Your own liability insurance that you pay for and that covers your work.

Your own branding — vest, vehicle decals, business card — visibly distinct from the GC.

You hire helpers (employees, T4A subcontractors). The PSB definition requires more than five full-time employees other than yourself to fail outright on condition 3 — but even one or two helpers shifts the integration factor materially.

You decline some work. A genuine independent contractor can say no. An incorporated employee can't.

None of these factors alone solves the problem. Together, they move the analysis.

The 80% rule of thumb

The CRA doesn't publish a hard percentage threshold, but auditors regularly note that an incorporated contractor with 80%+ of revenue from a single payor is a candidate for PSB classification. That's not a statutory cutoff — it's a pattern observation.

Two practical implications:

Monitor your client mix monthly. If one GC is creeping past 70%, plan to take on additional work or restructure how you bill the dominant client.

Don't accept "we'll just hire you as our incorporated sub" arrangements that have no other features of independent contracting. The GC isn't on the hook for PSB tax — you are. The arrangement that benefits them is sometimes the one that destroys your tax position.

What to do if you might already be a PSB

If you've been incorporated, invoicing one GC, billing hourly, using their tools, attending their meetings — and you suspect the CRA might reassess — the right move is preemptive:

Talk to a CPA before the CRA does. The Modern Axis tax planning team handles PSB risk assessment as part of structuring decisions.

Restructure the relationship. Take on additional clients, shift to fixed-price contracts, bring your own equipment back into the picture.

Consider the Voluntary Disclosures Program if you've already been assessed as employment-like by another tribunal or if you have other tax-position concerns. (See the Modern Axis VDP guide.)

When the PSB analysis lands on Contractor Tax Hub

Contractor Tax Hub flags PSB risk on incorporated-contractor onboarding — reviewing the four-factor profile, the client mix, and the engagement structure. If you're already at risk, the Premium package includes structural cleanup as part of the engagement; if you're a sole prop considering incorporation, talk to us before you incorporate. Once the structure is in place, the PSB risk follows it forward.

Frequently asked questions

What is a Personal Services Business?

Under Income Tax Act subsection 125(7), a Personal Services Business is a corporation whose business is providing services through an individual (an "incorporated employee") who would reasonably be regarded as an employee of the payor if the corporation didn't exist. The corporation can't claim the small business deduction, can't deduct most operating expenses, and pays the general corporate tax rate.

Why does the CRA care?

Without the PSB rules, an employee could "incorporate themselves," route their employment income through the corporation, claim the small business deduction (low tax rate), and use corporate deductions to shelter income — effectively cutting their personal tax rate dramatically. The PSB rules close that gap by stripping the SBD and most deductions when the corporation is just a tax-conduit for what's really employment. (Contractor Tax Hub's contractor-vs-employee primer is the broader companion if you're working through the employment-vs-self-employment question for the first time.)

What's the test for PSB classification?

A four-factor analysis from the common-law employee-vs-contractor test (Wiebe Door / Sagaz): control (who directs the work), ownership of tools (whose equipment), chance of profit and risk of loss (do you bear financial risk on the work), and integration (are you part of the payor's organization). No single factor is decisive; the whole picture decides.

I work for one GC for most of my time. Am I automatically a PSB?

Not automatically — but client concentration is the single biggest risk factor. An incorporated contractor with 80%+ of revenue from a single payor is a candidate for PSB classification when the other factors lean toward employment (hourly billing, GC-supplied tools, GC-set schedule, no independent risk). Diversifying your client mix is the most reliable way to move the analysis.

What expenses can a PSB still deduct?

Under Income Tax Act paragraph 18(1)(p), a PSB can deduct: salary and wages paid to the incorporated employee, the employer's portion of CPP/EI on that salary, certain travel expenses required to perform the services, expenses related to selling the services, and a narrow list of other specific items. Most ordinary operating expenses are denied.

What's the tax impact of PSB classification?

The corporation loses the small business deduction (federal goes from ~9% to 15%; BC provincial goes from ~2% to 12%). Combined: roughly 11 percentage points more corporate tax on every dollar of PSB-classified income. Plus the shareholder still pays personal tax on the salary they drew. The combined burden frequently exceeds what the same income would have attracted as straight employment income — making the corporation worse than useless for tax purposes.

Can the CRA reassess prior years?

Yes. The CRA can reassess within the normal reassessment period — typically three years from the original notice of assessment for CCPCs. Reassessments can go back further if gross negligence or misrepresentation is found. Most PSB reassessments cover the most recent three years.

How do I stay out of PSB classification?

Diversify clients (multiple genuine payors), use your own tools and equipment, accept fixed-price contracts where possible, carry your own liability insurance, present your own branding, hire helpers if practical, and be willing to decline work. None of these alone solves the problem — they shift the four-factor analysis together. Worth a conversation with a CPA before incorporation.

Is the PSB risk the same for sole proprietors?

No. PSB rules apply only to corporations. A sole proprietor providing services to a single client doesn't face PSB classification, but they can face a similar reassessment under the broader "employee vs. independent contractor" analysis (the CRA may reassess the relationship as employment, with consequences for the payor). The mechanics differ; the underlying question is the same.

This post covers general principles of the Personal Services Business rules in Canada. It is not advice for your specific business. PSB classification is fact-specific and depends on the full pattern of your engagement, not on any single factor. If you're an incorporated contractor with concentrated client revenue, talk to a CPA before the CRA does — the cleanup is dramatically easier when it's preemptive.