Trade Vehicle Deduction: Class 10 vs 10.1 + the Mileage Log

The CCA class your truck belongs in, the $39,000 cap, lease-vs-buy math, and what a CRA-defensible mileage log actually looks like.

Trade vehicle deduction in Canada: Class 10 vs 10.1, the $39,000 cap, lease vs buy, business-use mileage, and the CRA 12-month log rule.

The CRA's review letter arrives in March. They want a mileage log for the truck for the last two tax years. You have a dashboard photo of the odometer from January and a vague memory of "about half" being business. That's not what the auditor wants. The motor-vehicle expense line on your T2125 just got disallowed.

This post covers the trade vehicle deduction as it actually works for Canadian contractors in 2026 — which CCA class your truck belongs to, the $39,000 ceiling, lease vs buy, how to handle business-use percentage, and what a CRA-defensible mileage log actually looks like.

Key takeaways

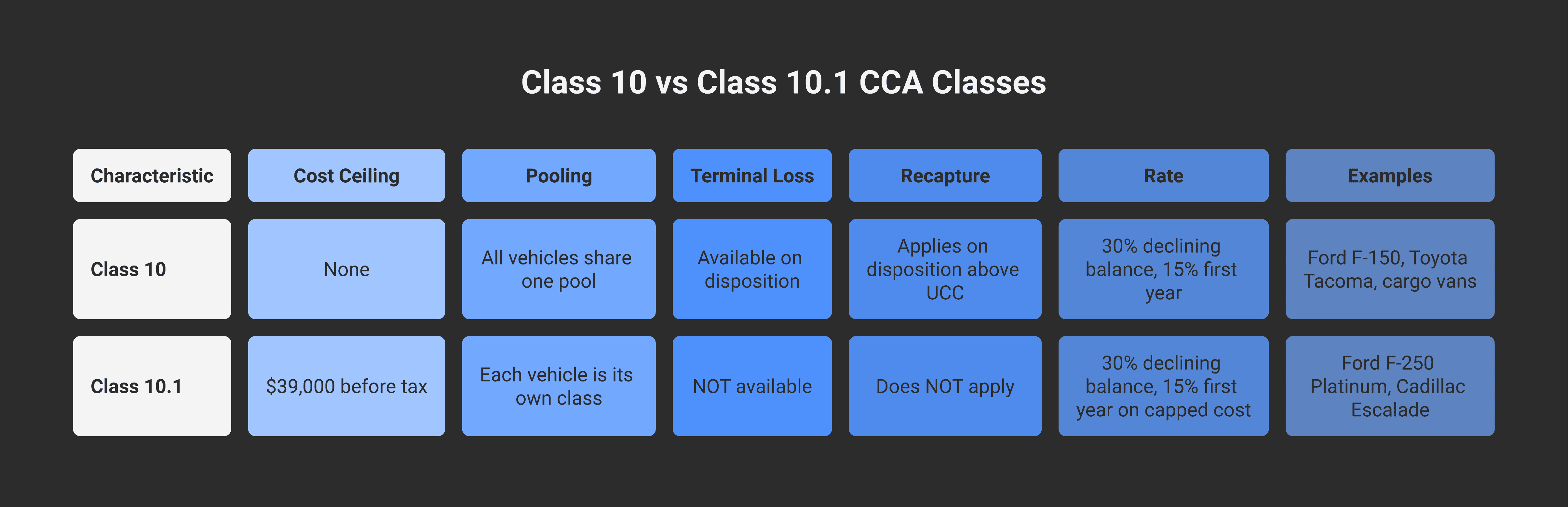

Most contractor trucks (Ford F-150s, half-tons, vans, pickup-cab-and-chassis combinations used in trades) cost under $39,000 before tax and go in Class 10 — pooled, 30% declining-balance CCA rate, 15% first-year claim (half-year rule).

Vehicles over $39,000 before tax that meet the "passenger vehicle" definition (most non-commercial pickups and SUVs in personal use) go in Class 10.1 — capped at $39,000 of CCA-able cost, each vehicle gets its own class, no terminal loss available on disposition.

Lease deduction cap for new leases on or after January 1, 2026: $1,100 per month before tax. The actual deductible amount is the lesser of two CRA formulas — bookkeeping software handles the math.

Business-use percentage is required. You can't deduct 100% of the truck unless 100% of the kilometres were business. The CRA accepts a 12-month representative logbook kept once, then ongoing estimates derived from that sample — but a logbook is the floor, not the ceiling, of audit defence.

Operating expenses (fuel, insurance, repairs, maintenance, parking, washes) are deductible at the business-use percentage. The CCA on the vehicle is also pro-rated by business-use percentage. (Modern Axis covers the broader vehicle-expense framework for rental-property and other business contexts.)

The rule, in one sentence

Under Income Tax Regulation Schedule II and the related sections, every motor vehicle you use for business is classified into a CCA class — Class 10 for most contractor work vehicles, Class 10.1 for "passenger vehicles" over the cost ceiling, Class 54 for zero-emission passenger vehicles. The class determines your CCA rate, the cost-base ceiling (if any), and whether you can claim a terminal loss on sale.

The choice isn't yours to make. It follows the vehicle type, cost, and use.

Class 10 — most contractor trucks

If you bought a truck for $39,000 or less before tax that is used in your business, it's almost certainly in Class 10.

Class 10 properties:

Rate: 30% declining balance (15% in the year of acquisition due to the half-year rule)

Pooling: all your Class 10 vehicles are in a single pool. Add one, subtract the original cost when you sell, calculate CCA on the pool balance.

Terminal loss available: if the pool balance goes negative when you dispose of a vehicle (sold for less than its undepreciated cost), you can claim the difference as a terminal loss in that year.

Recapture applies: if you sell a vehicle for more than its undepreciated cost in the pool, the difference is added back as income (recapture).

Examples: Ford F-150, Ford Ranger, Toyota Tacoma, Chevrolet Silverado 1500, GMC Sierra, Dodge Ram 1500, most cargo vans, work vans, half-ton pickups under the cost ceiling.

A used vehicle bought below the ceiling is also Class 10. Trade-in value counts toward the cost calculation for the ceiling test.

Class 10.1 — the $39,000 cap

If you bought a vehicle that meets the passenger vehicle definition AND costs more than $39,000 before tax (for vehicles acquired in 2026), it's in Class 10.1.

Class 10.1 properties:

Cost ceiling: $39,000 for 2026 acquisitions (increased from $38,000 in 2025). The CCA is calculated on this capped cost, not the actual purchase price.

Rate: still 30% declining balance, 15% first year.

Each vehicle is its own separate class. No pooling. You track each Class 10.1 vehicle's UCC individually.

No terminal loss available. When you dispose of a Class 10.1 vehicle, you can't claim a loss if you sell below the UCC. The loss is gone.

Recapture doesn't apply. Sell above UCC and you don't get hit with recapture income. (One small mercy.)

Examples: Ford F-250 or F-350 in higher trims, Toyota Tundra Limited / Platinum, Cadillac Escalade, GMC Yukon Denali — most $40K+ pickups and SUVs in non-commercial trim used by a sole-prop trade.

The 50%-business-use exemption: a pickup truck is not treated as a passenger vehicle (and so escapes the Class 10.1 ceiling) if it is used more than 50% of the kilometres for business AND has either: (a) a seating capacity of 3 or fewer including driver, OR (b) is used to transport goods/equipment in the course of earning income. Most working pickups meet condition (b). When the exemption applies, an expensive pickup goes in Class 10 — no $39,000 cap.

This exemption is the single most important rule for tradespeople buying $50,000+ pickups. With proper documentation (logbook + business-use evidence) the entire purchase price goes into Class 10 and depreciates at the full 30% rate. Without it, you're stuck at the $39,000 ceiling.

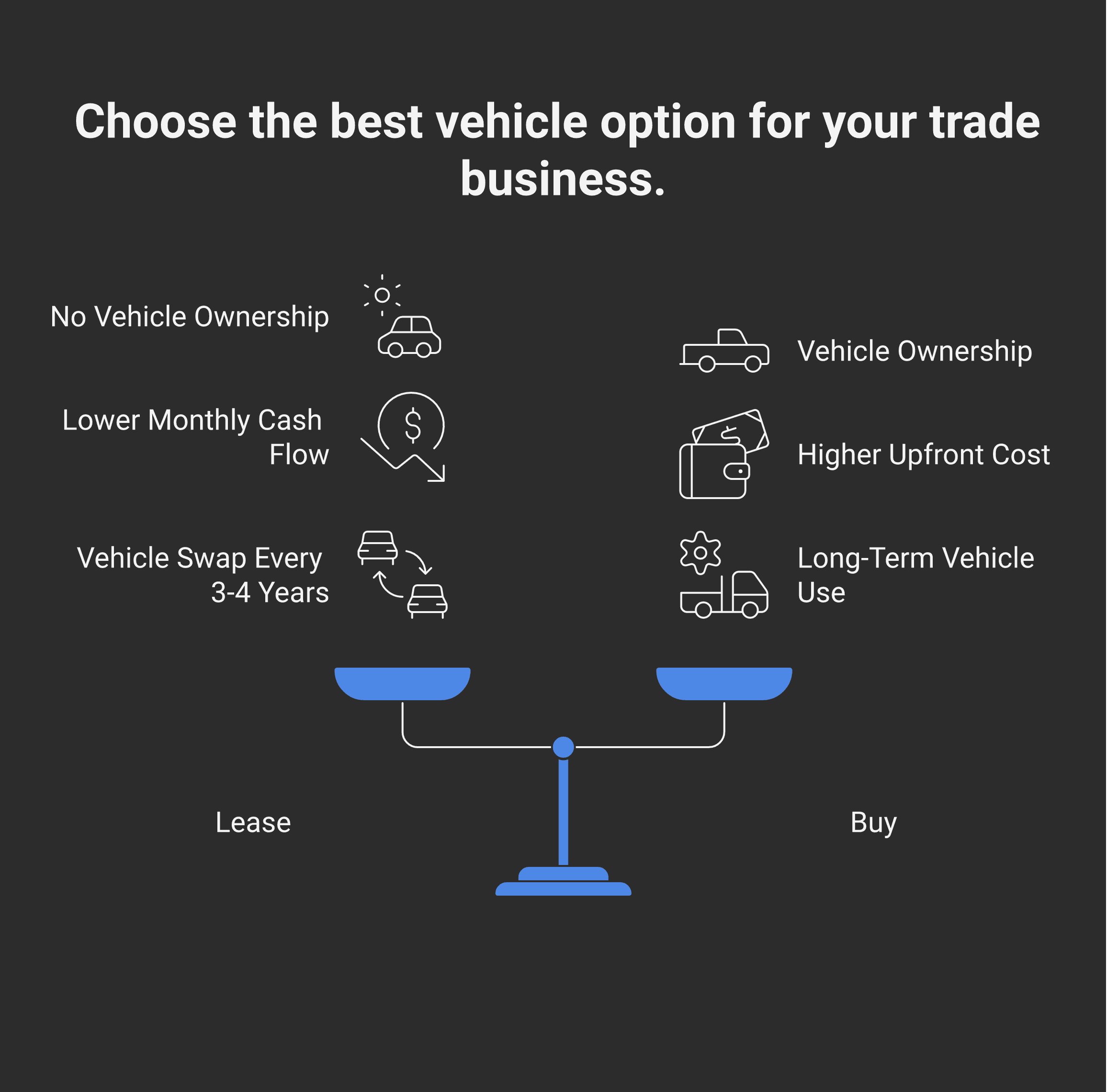

Lease vs buy

Two different deduction mechanics:

Lease

The CRA caps monthly lease payments that can be deducted. For new leases entered into on or after January 1, 2026, the cap is $1,100 per month before tax (up from $1,050 in 2025). The actual deductible amount is the lesser of:

The actual monthly lease payment, OR

A formula amount that limits the deduction based on the vehicle's manufacturer's list price relative to the prescribed cap.

The full formula is in Regulation 67.3 of the Income Tax Act and is automatically applied by QuickBooks, Sage, and most payroll software. The practical effect: lease a $60,000 vehicle and you can't deduct the full $1,500/month payment — the formula limits you to $1,100/month effective.

GST/HST on the leased portion is creditable as an ITC at the business-use percentage (regular method) or as a capital-purchase ITC (Quick Method).

Buy

You add the vehicle's cost to the appropriate CCA class and depreciate. No monthly cap (for Class 10); the $39,000 cap for Class 10.1.

Buying lets you eventually own the vehicle and stop paying for it. Leasing keeps the monthly cost lower (often) but you never own it. For trade businesses where the truck is the primary work asset, buying-and-owning is usually the long-game answer. For businesses that want to swap trucks every 3-4 years (matching contracts or fleet operations), leasing can be cleaner.

The decision usually turns on cash-flow and how long you plan to hold the vehicle, not on tax alone. A bookkeeper or Modern Axis CPA on the planning side can run the math for your specific situation — particularly important if you're considering incorporation (the answer can change at the corporate level).

Business-use percentage and the mileage log

You can only deduct the business-use portion of a vehicle's expenses and CCA. The CRA's standard for proving business-use percentage is a mileage logbook — and they've published clear guidance.

What the CRA accepts

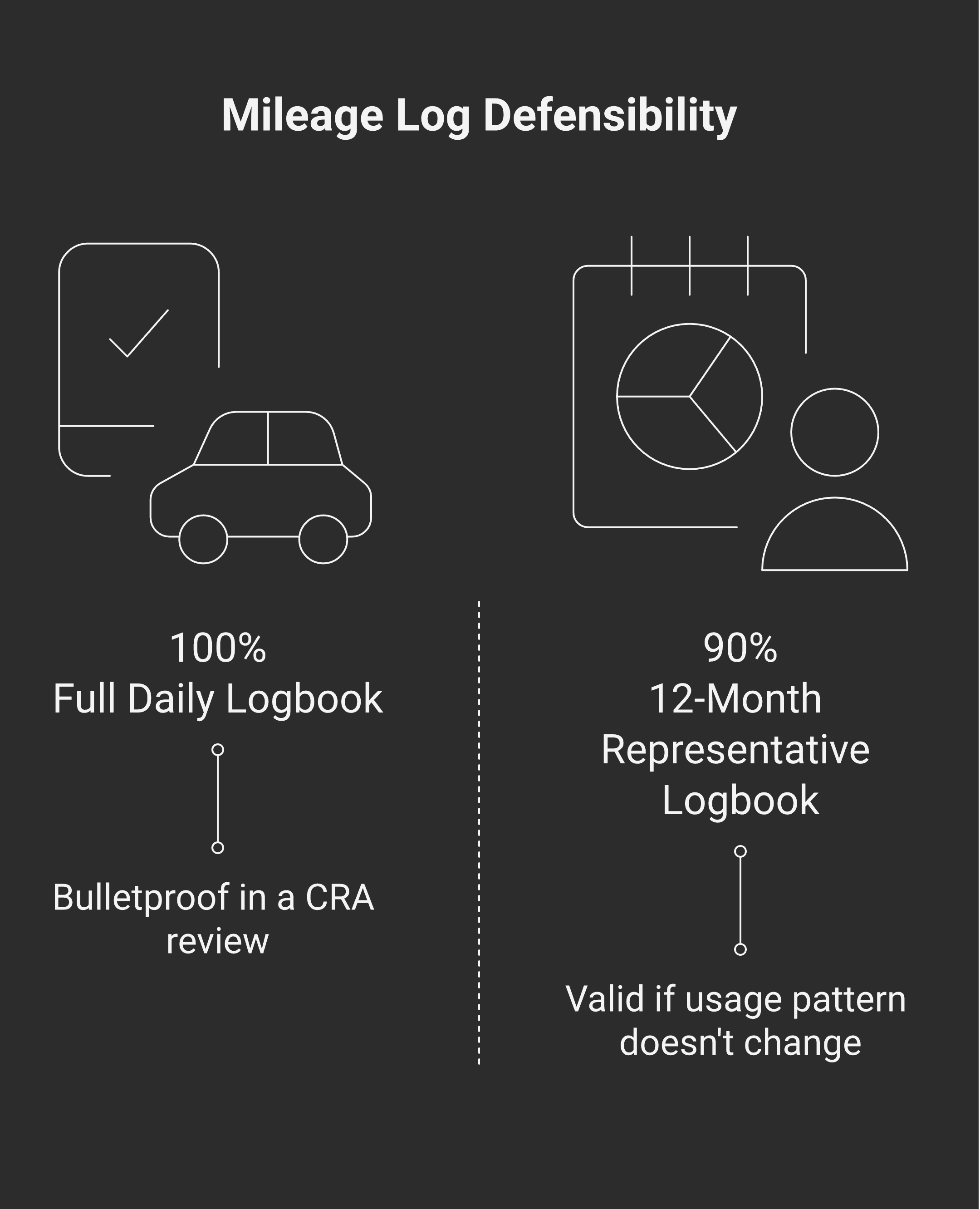

The CRA's official position (from CRA Folio S2-F3-C2 and related guidance) is that you can either:

Keep a full daily logbook, recording each trip: date, destination, purpose, starting odometer, ending odometer; OR

Keep a 12-month representative logbook, then use it as the basis for ongoing estimates in subsequent years as long as your business-use percentage doesn't change by more than 10% year over year.

The 12-month representative logbook is the practical standard for ongoing operations. You keep meticulous records for 12 consecutive months, calculate your business-use percentage (let's call it 78%), and then use that 78% going forward — provided your usage patterns are stable.

If your usage changes materially (you take on a long-distance client, you start commuting from a new home base, you reduce the personal use significantly), you need a fresh 12-month logbook.

A modern mileage app (QuickBooks Mileage tracking, MileIQ, TripLog) is the most defensible approach. The app captures every trip automatically via GPS; you classify each trip as business or personal at the end of the day; the app generates an audit-ready report at year-end.

What the CRA doesn't accept

"About half" or "approximately 70%" business use, without records

Estimates based on a single typical week, projected over a year

A logbook reconstructed after the fact (especially if a review letter has already arrived)

Records that don't tie to actual odometer readings

The single most expensive vehicle-deduction outcome in trades is having the full motor-vehicle expense line disallowed on a CRA review. That happens when there's no logbook and no other corroborating evidence. The vehicle goes from a major deduction to zero, with interest and penalties on the reassessed tax.

Operating expenses

In addition to CCA, you deduct operating expenses at the business-use percentage:

Fuel — gasoline, diesel, propane

Insurance — vehicle insurance premium

Repairs and maintenance — oil changes, brake jobs, tire replacement, body work

Licence and registration — annual ICBC fees in BC

Interest on the vehicle loan — capped at $350/month for purchases on or after January 1, 2024

Parking — when business-related; reasonable client-visit parking is fully deductible regardless of overall vehicle business-use %

Car wash — when reasonable for business presentation

Roadside assistance — CAA or equivalent

Toll and parking receipts at customer sites are fully deductible (they're job-specific business expenses regardless of overall vehicle business-use percentage). Other expenses get pro-rated.

GST/HST on all of these is creditable as ITC at the business-use percentage (regular method only — Quick Method electors lose ITCs on operating expenses).

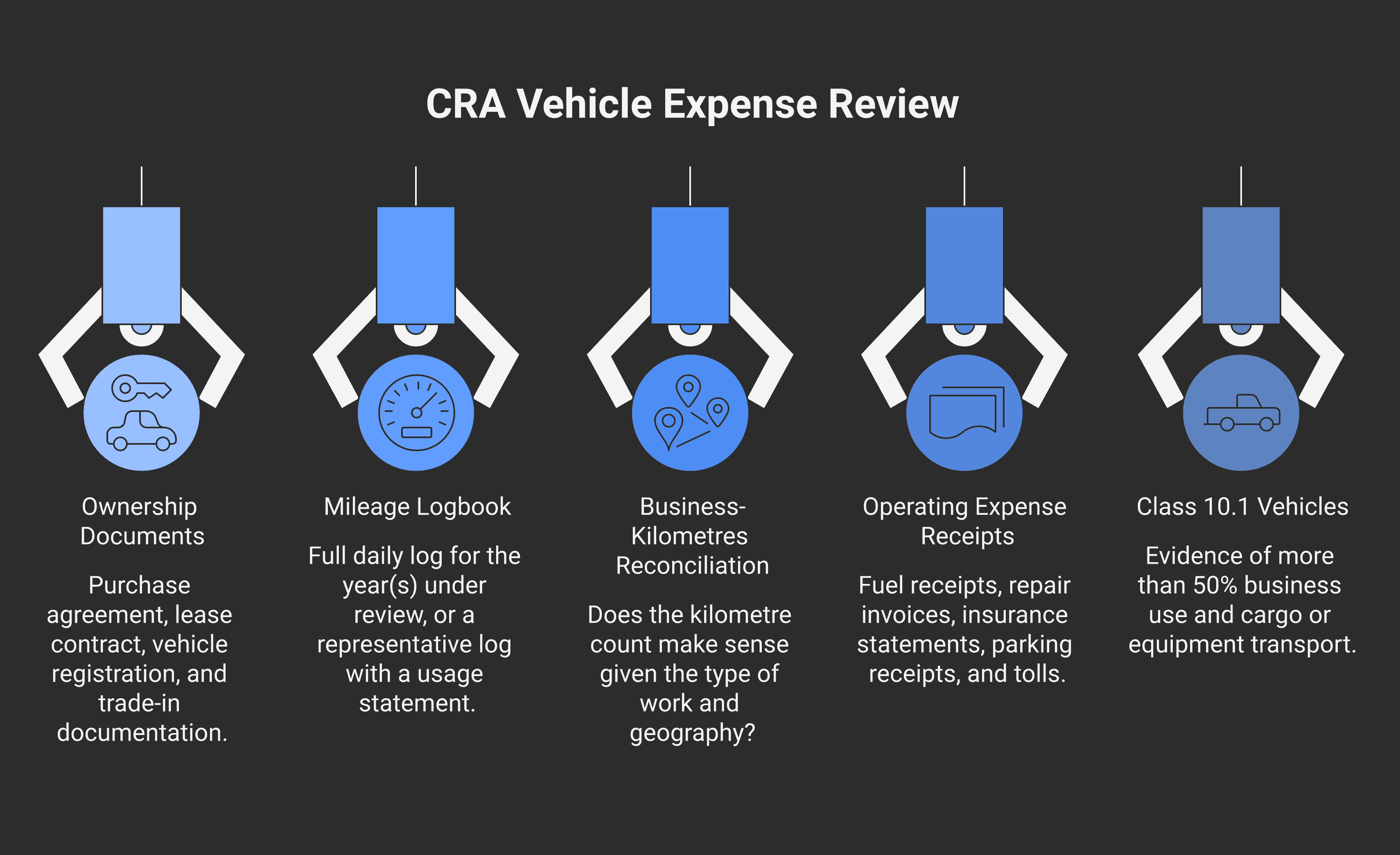

What the CRA actually looks for in a review

The motor-vehicle line is one of the most frequently reviewed deductions on a contractor's T2125 (sole prop) or T2 (corporation). When the review letter lands, the CRA typically asks for:

The vehicle ownership documents (purchase agreement, lease contract, registration)

The mileage logbook for the year(s) under review (or the 12-month representative log plus your usage statement)

A reconciliation of business kilometres to gross income — the CRA's first sanity check: does the kilometre count make sense given the kind of work and the geography?

Receipts for the operating expenses claimed — fuel, repairs, insurance, parking

For Class 10.1 / passenger vehicles: proof that the 50%-business-use + cargo-transport exemption applies (if claimed)

The cleanest defence is the full set of contemporaneous records. Bookkeeping software (Dext or HubDoc for receipt capture) plus a mileage app plus a tidy QuickBooks file usually clears a review in days. The opposite — no logbook, scattered receipts, no reconciliation — usually ends with the deduction disallowed.

When the vehicle deduction lands on Contractor Tax Hub

Contractor Tax Hub handles the CCA pool calculation, the Class 10 vs 10.1 determination, the lease-vs-buy math, the mileage-log integration with QuickBooks, and the year-end review of business-use percentage as part of every monthly engagement. The Starter and Growth packages include this; if you've been claiming "approximately 70%" without a log and a review letter has arrived, talk to us before responding.

Frequently asked questions

What CCA class is my truck in?

Most contractor work trucks costing $39,000 or less before tax go in Class 10 — 30% declining balance, pooled, terminal loss available on disposition. Vehicles over $39,000 that meet the "passenger vehicle" definition go in Class 10.1 — capped at $39,000 of cost, each its own class, no terminal loss. The pickup-truck exemption (more than 50% business use + transporting goods/equipment) lets expensive pickups stay in Class 10.

What's the difference between Class 10 and Class 10.1?

Cost-base ceiling: Class 10 has no ceiling; Class 10.1 caps cost at $39,000 (2026). Pooling: Class 10 vehicles share one pool; each Class 10.1 vehicle is separate. Terminal loss: available for Class 10, not Class 10.1. Recapture: applies to Class 10, not Class 10.1. Both depreciate at 30% declining balance, 15% first year.

What's the lease deduction limit for 2026?

For new leases entered into on or after January 1, 2026, the cap is $1,100 per month before tax (up from $1,050 in 2025). The actual deductible is the lesser of the actual lease payment and a formula amount based on the vehicle's MSRP relative to the prescribed cap. The full math lives in Regulation 67.3.

Do I need a mileage log?

Yes. The CRA's standard is either a full daily log or a 12-month representative log used as the basis for ongoing estimates (provided your business-use percentage doesn't change by more than 10% year over year). Modern apps like QuickBooks Mileage, MileIQ, or TripLog capture trips automatically via GPS — the most defensible setup.

What if I bought a $60,000 pickup truck?

It depends on use. If the truck is used more than 50% of its kilometres for business AND transports goods or equipment in the course of earning income, it qualifies for the pickup-truck exemption and goes in Class 10 (full cost depreciable, 30% rate, no ceiling). Without the exemption, it's Class 10.1 capped at $39,000 of cost.

Can I deduct car washes and parking?

Yes. Car washes are deductible at the business-use percentage (the same percentage you use for fuel and insurance). Parking is deductible at the business-use percentage for general parking, and fully deductible for trip-specific parking at customer or supplier sites (that's a direct business expense, not a vehicle expense subject to pro-rating).

What's the home-to-jobsite commute rule?

Travel from home to a fixed regular workplace (your shop, your office, your usual main jobsite) is personal kilometres, not business. Travel between jobsites during the day is business. Travel from home to a temporary or specific jobsite (varying by project) can qualify as business if the home is your real principal place of business (genuine home office) — but this is a fact-specific question and worth a conversation with your bookkeeper or CPA.

What happens if I can't produce a logbook in a CRA review?

The CRA will typically disallow the motor-vehicle expense line entirely, reassessing the tax, interest, and possible penalties. The cleanest recovery path is to reconstruct as much contemporaneous evidence as possible (calendar appointments, job photos with timestamps, customer invoices showing site addresses, GPS history if available) and submit a reasoned business-use estimate. Outcomes vary; the burden of proof is on you.

This is a general overview of how the trade vehicle deduction works in Canada in 2026, not advice for your business. CCA classes, lease caps, and exemption rules change between tax years, and the right answer for your specific vehicle, use pattern, and business structure depends on facts not covered above. Contractor Tax Hub can look at your specific numbers — but don't rely on a blog post in place of that.