GST Registration for Tradespeople: The $30K Rule

When to register, when to elect Quick Method, and the ITC math that decides whether you pocket the difference.

GST registration for tradespeople — when you cross the $30,000 threshold, the Quick Method election, and the ITC math on tools and trucks.

You crossed $30,000 in revenue sometime in October. You didn't notice. The CRA did. By the time you realize you should have registered for GST, you owe the tax on every dollar you've billed since the threshold crossed — to subs, to homeowners, to the general contractor — even though you never collected it.

This post covers when GST registration is required for Canadian tradespeople, how the four-quarter clock works, when voluntary registration makes sense, the Quick Method election (and the math that decides whether it pays off for trades), and what input tax credits actually let you claim on tools and trucks.

Key takeaways

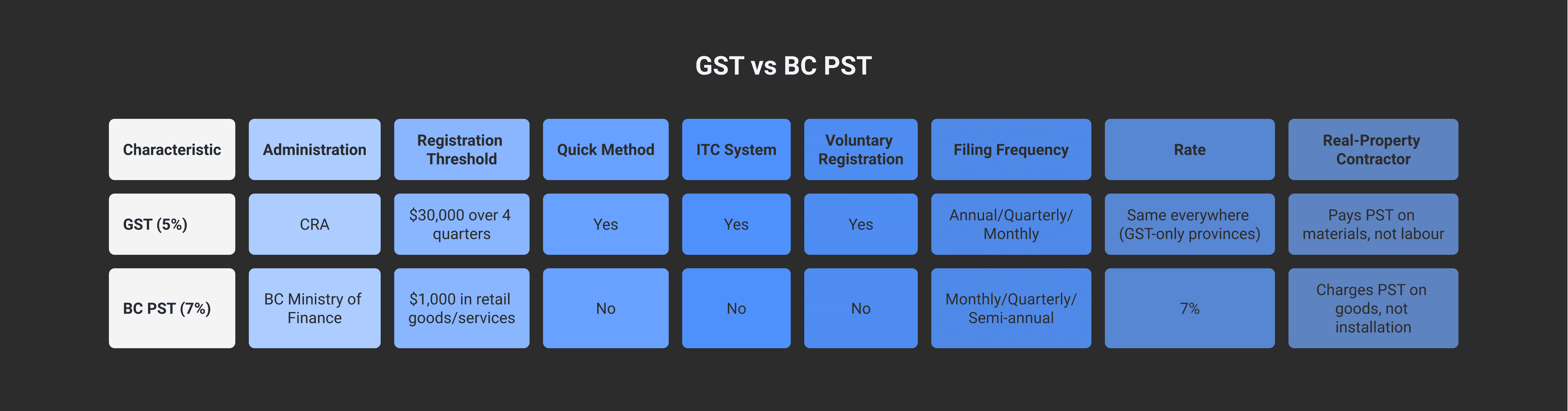

The CRA's "small supplier" threshold is $30,000 in total taxable revenue over four consecutive calendar quarters (not the calendar year). Cross the threshold and registration is required starting the day after.

Voluntary registration before $30K is allowed and sometimes worth it — you can claim input tax credits on tools, vehicle expenses, and capital purchases, which a non-registrant cannot.

The Quick Method (Form GST74) lets BC service-trade businesses collect 5% GST but remit a reduced rate (around 3.6% of revenue-including-GST), pocketing the difference. The trade-off: no ITCs on regular operating expenses, only on capital purchases.

Quick Method rates depend on your province and supply mix. For BC tradespeople providing services in a GST-only province, the rate is roughly 3.6%; if you sell goods or HST-province services, different rates apply. (CRA's RC4058 guide is the authoritative source.)

BC PST is a separate problem. BC charges 7% PST on top of 5% GST. PST registration follows different rules (separate threshold, separate filing, no equivalent of Quick Method). If you install materials in BC, you may owe PST regardless of your GST status.

The rule, in one sentence

If your business has earned $30,000 or more in total worldwide taxable revenue over any four consecutive calendar quarters (the most recent four, rolling), you are no longer a small supplier and you have to register for GST/HST immediately. From that day forward you charge GST on every taxable supply — and from the date of crossing forward, you owe the CRA the GST whether you collected it or not.

The threshold is per business, not per project or per client. A framing sub on residential and a separate landscaping side-business count as one business for the threshold if they're operating under the same business number.

The four-quarter clock — and how it starts

The four consecutive calendar quarters mean the most recent four, rolling. Quarters are calendar quarters (Q1: Jan-Mar, Q2: Apr-Jun, Q3: Jul-Sep, Q4: Oct-Dec), not your fiscal-year quarters.

Two ways to cross the threshold:

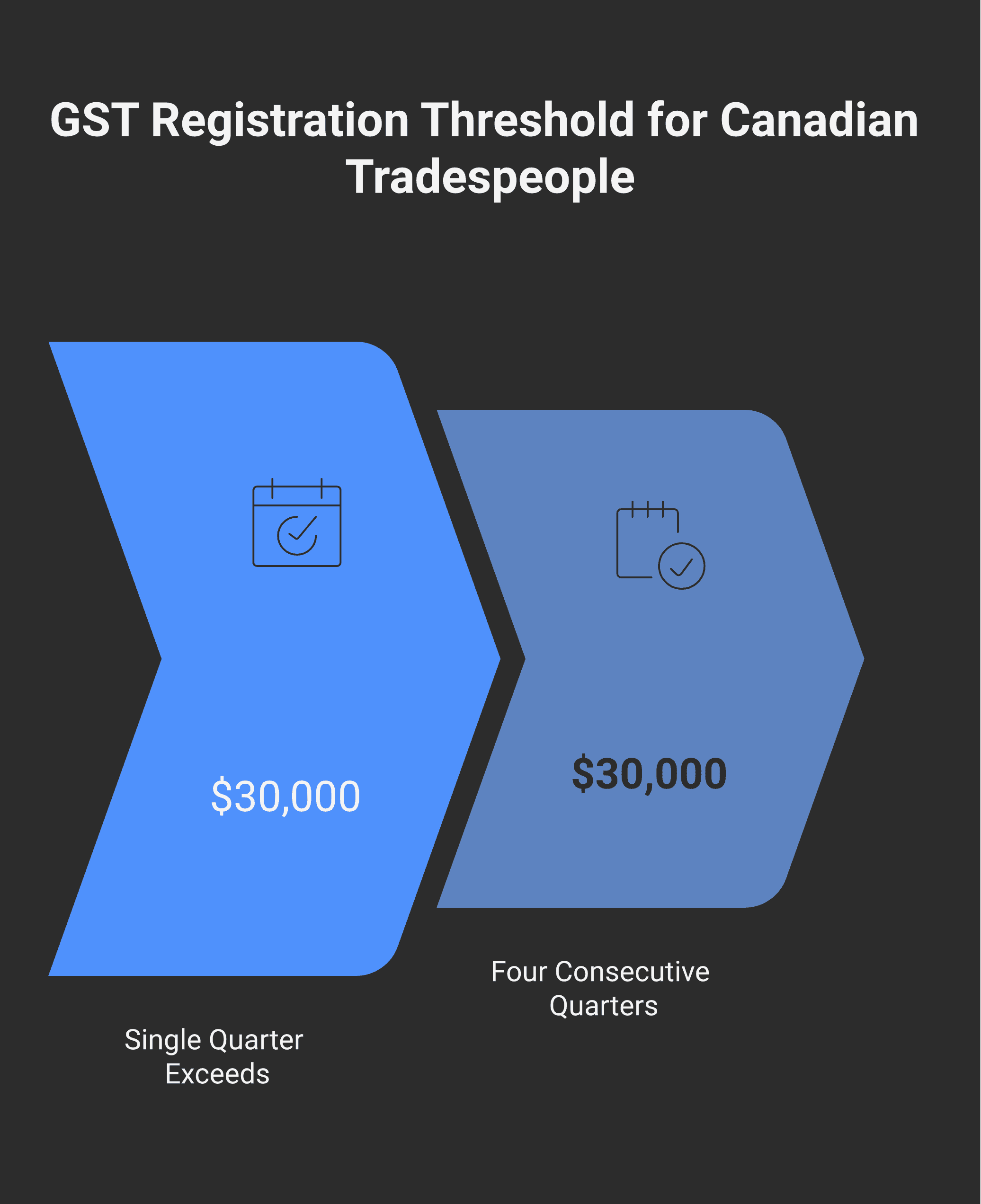

Way 1 — single quarter over $30,000. If you earned more than $30,000 in any single calendar quarter, you stop being a small supplier on the first day of the second month after that quarter. You must register and start charging GST from that date.

Way 2 — four-quarter total over $30,000. If your most recent four consecutive calendar quarters total more than $30,000, you stop being a small supplier on the day after the end of those four quarters. Register and start charging from that day.

In practice, most tradespeople cross the threshold via way 2 — a gradual accumulation rather than a single big quarter. Bookkeeping needs to track rolling four-quarter revenue every quarter-end so you know when the threshold is crossing. (CTH's tax write-offs guide covers the bookkeeping setup that surfaces this in time.)

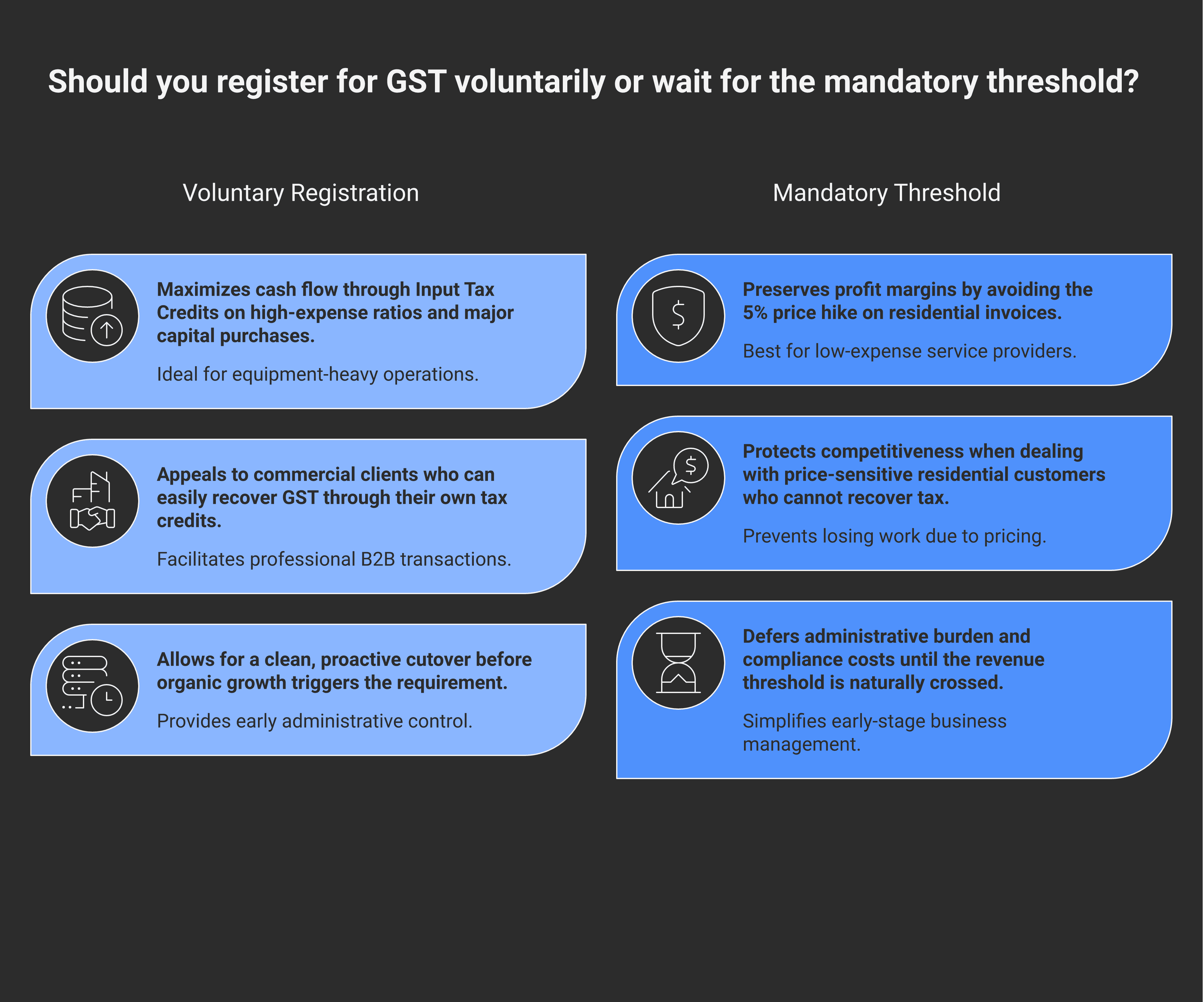

Voluntary registration before $30,000

You can voluntarily register for GST before crossing $30,000. The trade-off:

Pro: you can claim input tax credits (ITCs) on the GST you pay on business expenses — tools, materials, vehicle fuel, vehicle purchase, gas, software, insurance, supplies. ITCs offset GST you collect or get refunded if you collect less than you spent.

Pro: you look more established to commercial clients (some GCs won't hire unregistered subs because the invoicing math is messier).

Con: you now have to charge GST on every invoice. Residential clients (where GST is end-cost, not creditable) may shop competitors who aren't registered.

Con: you have to file returns. Even a nil return for a quiet quarter takes time.

When voluntary registration usually wins:

You've bought a truck or major tools and the ITCs on those purchases beat the administrative cost of being registered.

All or most of your clients are GCs or businesses that recover the GST through their own ITCs. They don't care about the extra 5% on your invoice.

You're approaching $30K and want a clean cutover rather than a mid-quarter registration scramble.

When voluntary registration usually loses:

You're a residential-only contractor at $15-20K of revenue with minimal capital purchases.

Your expenses are low relative to revenue (services with minimal materials).

You'd rather wait until you cross the threshold organically.

Either way, the GST you collect doesn't change your income tax picture — GST is a separate tax flow. The income tax mechanics for sole-prop tradespeople live in Modern Axis's personal income tax guide, and the corporate-side picture (if you've incorporated) shows up on the T2 alongside the small business deduction.

The Quick Method — and the math that decides for trades

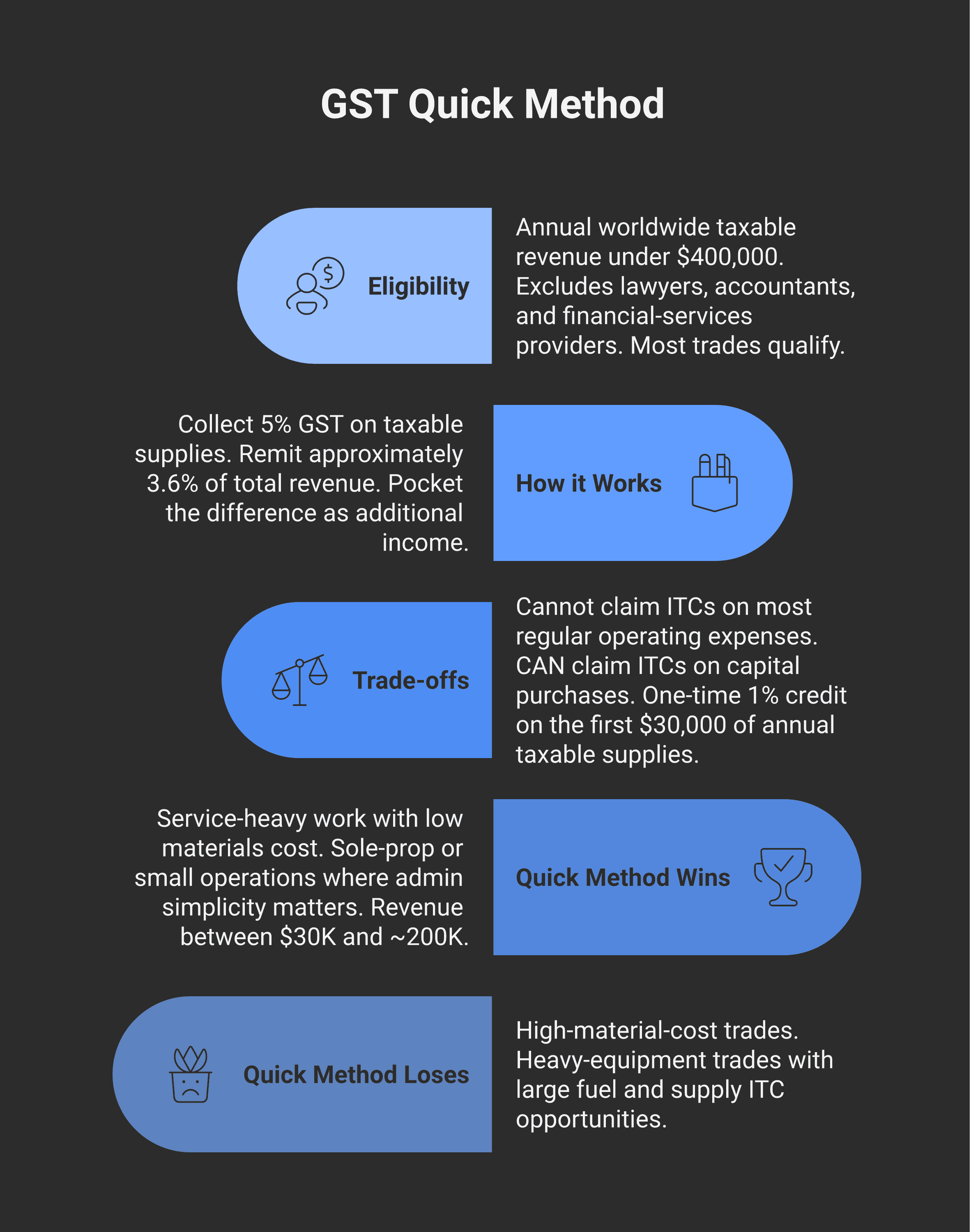

The Quick Method (Form GST74) is an election available to most small registrants. Eligibility: annual worldwide taxable revenue (including GST/HST) under $400,000. Lawyers, accountants, and financial-services providers are excluded — most trades qualify.

How it works for a BC service-trade business:

You collect the regular 5% GST on every taxable supply.

You remit a reduced rate to the CRA — for a BC service-trade in a GST-only province, the published rate is approximately 3.6% of total revenue (including the GST collected).

The difference is yours to keep — effectively additional income, taxed as business income on your T1 or T2.

The trade-off: when you're on the Quick Method, you cannot claim ITCs on most regular operating expenses (tools, vehicle fuel, materials, supplies, software). You CAN still claim ITCs on capital purchases (vehicle purchase, large equipment over a single-purchase threshold). Everything else's GST stays as a cost.

When the Quick Method wins for trades:

Service-heavy work with low materials/expense ratios (finishing trades, repairs, small-scale work where labour is most of the bill)

Sole-prop or small operations where the administrative simplicity matters

Revenue between $30K and ~$200K where the math works out cleanly

When the Quick Method loses for trades:

High-material-cost trades where the lost ITCs exceed the rate savings (framing with bulk lumber purchases, roofing with material-heavy contracts)

Heavy-equipment trades where vehicle fuel and supplies create large ITC opportunities

Larger operations where bookkeeping handles regular-method GST without much added overhead

There's a one-time 1% credit on the first $30,000 of your annual taxable supplies in each fiscal year when you use the Quick Method. That's a small but real bonus for tradespeople just past the registration threshold.

The election effective date must be the first day of a GST/HST reporting period. You cannot retroactively elect into the Quick Method mid-quarter.

Input tax credits on tools and trucks (when you're on regular method)

If you stick with the regular method (or you're voluntarily registered and below Quick Method consideration), ITCs are the reason. You claim back the GST you paid on legitimate business expenses:

Tools — power tools, hand tools, tool storage, tool boxes mounted on the truck

Vehicle fuel — pro-rated to business-use percentage with a proper mileage log

Vehicle purchase or lease — pro-rated to business-use percentage (subject to vehicle cap rules)

Materials — anything you install or consume on a project

Subcontractor invoices — if the sub is GST-registered, you claim back their GST

Workshop and office — rent, utilities, software, insurance (business-use portion only)

Trade certifications, courses, professional dues — yes (business-purpose only)

The biggest ITC misses on a typical contractor file:

Personal-use portion of a vehicle (you can't claim ITCs on the kid-and-soccer-gear half of the truck's gas)

Tools purchased before registration (no ITC because you weren't registered yet — unless you elected back-dated registration)

Mixed-use cellphone and internet (business-use percentage only, documented)

Filing frequency

Filing frequency is assigned by the CRA based on annual taxable revenue:

Annual taxable revenue | Default filing frequency |

|---|---|

Up to $1.5M | Annual (can elect quarterly or monthly) |

$1.5M – $6M | Quarterly (can elect monthly) |

Over $6M | Monthly |

Most small trades businesses are on annual filing — return + remittance due 3 months after fiscal year-end. Some elect quarterly to spread the cash-flow hit. Few small trades file monthly.

BC PST is a separate problem

GST is federal. BC PST is provincial. They are separate registrations, separate returns, separate rate structures, and not interchangeable.

BC charges 7% PST on most retail sales of goods. If you install materials at a customer's site as part of a construction project, the PST treatment depends on the project type and whether you're considered a "real-property contractor" or a "retailer of goods":

A real-property contractor installing materials into a building typically pays PST as the consumer when buying the materials, but does not charge PST on the labour or the installed materials to the customer. The PST is built into the contract price.

A retailer of goods installing those goods (e.g., appliance sales + installation) typically charges PST on the goods portion of the invoice.

This distinction is BC-specific and trades-trap territory. Worth a separate conversation with your bookkeeper or Modern Axis CPA on the planning side when you're working on jobs that involve significant material installation.

When the GST registration timing lands on Contractor Tax Hub

Contractor Tax Hub handles the rolling four-quarter monitoring, the registration mechanics, the Quick Method election (with the math up-front so you can see whether it pays off for your specific revenue and expense ratio), and the quarterly/annual GST returns. If you're approaching $30K or just past it, the Starter or Growth packages include the registration and ongoing returns. Book a call before the threshold crosses — registering after the fact means owing GST on revenue you never collected.

Frequently asked questions

When do I have to register for GST as a tradesperson?

When your total worldwide taxable revenue over any four consecutive calendar quarters reaches $30,000. The clock is rolling — track it every quarter-end. Crossing the threshold makes you a registrant on the first day of the second month after that quarter (if a single quarter exceeds $30K) or the day after the end of the four consecutive quarters (if the cumulative crosses).

Can I register for GST voluntarily before I hit $30,000?

Yes. Voluntary registration lets you claim input tax credits on business purchases (tools, vehicle, materials, fuel) which a non-registrant cannot. The trade-off is that you have to charge GST on every invoice, which can put off residential clients. Voluntary registration wins for high-expense trades, commercial-only contractors, or anyone with a recent major capital purchase.

What's the Quick Method and how does it work?

The Quick Method (Form GST74) is an election that lets you collect the standard 5% GST but remit a reduced rate (around 3.6% for BC service-trade businesses in a GST-only province) — pocketing the difference. The trade-off: you can't claim ITCs on most regular operating expenses, only on capital purchases. Effective date must be the first day of a reporting period.

Should I elect the Quick Method?

Depends on your expense ratio. Service-heavy trades with low material costs (finishing trades, repairs) typically win on Quick Method. High-material-cost trades (framing with bulk lumber, roofing with material-heavy contracts) typically lose because the foregone ITCs exceed the rate savings. Run the math on your last 12 months of revenue and expenses before electing.

Can I claim GST back on my tools and truck?

Yes, if you're registered. Tools (power tools, hand tools, storage), vehicle fuel (pro-rated to business-use), and vehicle purchase or lease (pro-rated, subject to cap rules) all generate input tax credits. You need a proper mileage log to prove business-use percentage on the truck. Quick Method electors lose ITCs on most operating expenses but keep them on capital purchases like a new truck.

What's the difference between GST and BC PST?

GST is federal (5%, administered by the CRA). PST is provincial (7% in BC, administered by the BC Ministry of Finance). They are separate registrations with separate returns. As a real-property contractor in BC, you typically pay PST on materials you buy and don't charge PST to customers — but the rule depends on the project type and your role in the supply chain.

Do I have to file monthly?

Most small trades file annually. CRA's default frequency is based on your annual taxable revenue: up to $1.5M is annual; $1.5M–$6M is quarterly; over $6M is monthly. You can voluntarily elect a more frequent schedule (quarterly or monthly) to spread the cash-flow impact.

What happens if I don't register but I should have?

The CRA assesses you for the GST you should have collected on every taxable supply from the date you crossed the threshold. You owe that GST whether or not you actually collected it from customers. Penalties apply for late filing, and interest runs from the original due dates. The clean catch-up is to register now with a back-dated effective date that matches your actual threshold-crossing date and to file the missing returns voluntarily — talk to a CPA before doing this on your own.

This is a general overview of how GST registration works for Canadian tradespeople, not advice for your business. The Quick Method math, PST treatment, and the right cutover date depend on facts not covered above. Contractor Tax Hub can run the numbers for your specific situation — but don't rely on a blog post in place of that.