T5018 Slip: Who Files, What Counts, and the $500 Rule

The construction-services slip every general contractor files and every subcontractor should care about.

T5018 explained for Canadian construction: the $500 per-sub threshold, the 6-month deadline, the cross-reference, and the $25-per-day penalty.

It's June 30. Your fiscal year ended December 31. The T5018 deadline was 12 days ago. You didn't file. You're now accumulating $25 per day per slip in late penalties, and you don't have a complete list of every sub you paid last year.

This post covers what the T5018 Statement of Contract Payments actually is, who has to file one, what counts as a construction service, the $500-per-sub threshold, the 6-month deadline, and what to do if you're already behind. (Our complete contractor-taxes-in-Canada guide is the broader companion if you need the full picture.)

Key takeaways

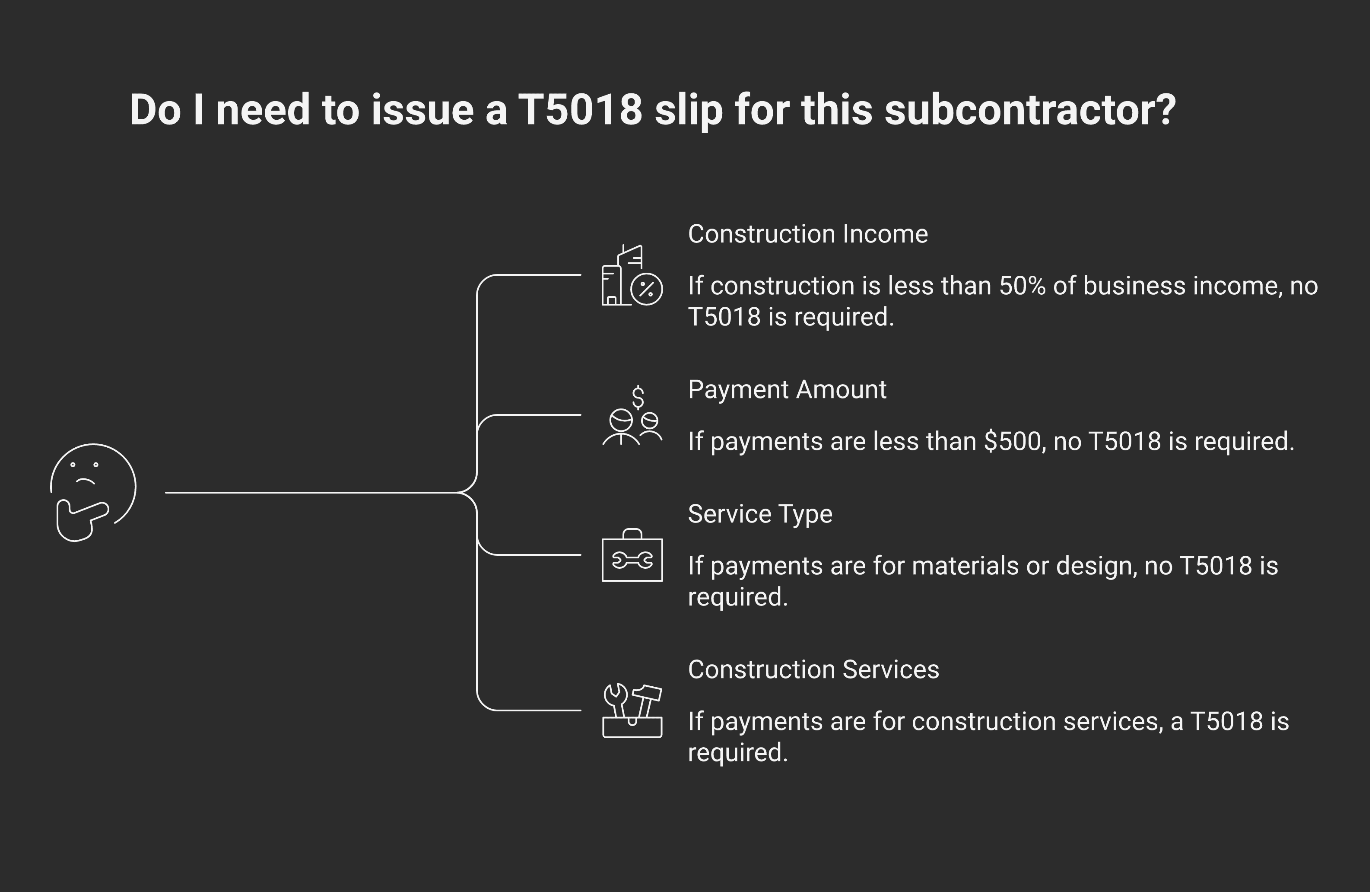

The T5018 is the slip Canadian construction businesses file to report payments made to subcontractors. Required when construction is more than 50% of your business income and when you paid any individual sub $500 or more in the reporting period (including GST/HST).

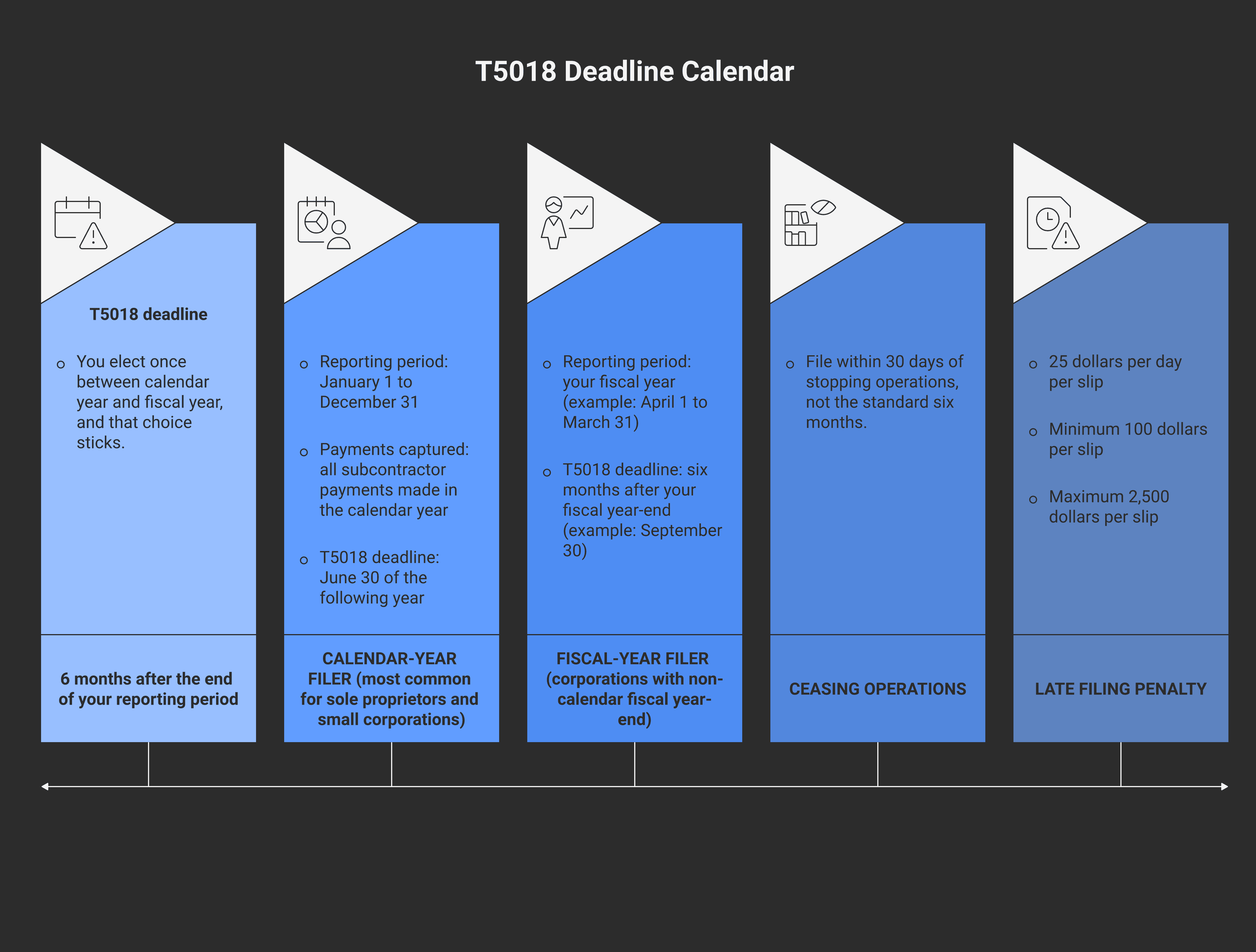

The deadline is six months after the end of your reporting period. You elect calendar year or fiscal year once — and you're stuck with that choice. December 31 year-end means a June 30 deadline. June 30 fiscal year-end means a December 31 deadline.

The penalty is $25 per day per unfiled slip, minimum $100, maximum $2,500 per slip. Miss 20 subs by 60 days and you're looking at a five-figure penalty before the file even gets reviewed.

The CRA cross-references the totals you reported on T5018s against each sub's reported income on their T1 or T2. A mismatch on either side is one of the cleanest audit triggers in the system.

Online filing is required if you're filing 6 or more slips for the 2025 tax year onwards (the threshold dropped from 50 in prior years).

The rule, in one sentence

Under the Income Tax Act's information-return rules and CRA's T5018 administrative guidance, if your business has more than 50% of its income-earning activity in construction, and you paid any subcontractor $500 or more during the reporting period for construction services, you have to issue that sub a T5018 slip and file the matching summary with the CRA — within six months of your year-end.

That obligation kicks in the moment you write the cheque. It doesn't matter whether the sub is incorporated, registered for GST, has their own tools, or works for ten other generals. If they're a sub on your project and you paid them more than $500 in the year, the T5018 follows.

Who files — and what construction means

The T5018 obligation applies if more than 50% of your business income comes from construction. That puts general contractors, builders, framing crews, electrical contractors, plumbing companies, roofers, finishing trades, and any related contractor squarely in scope.

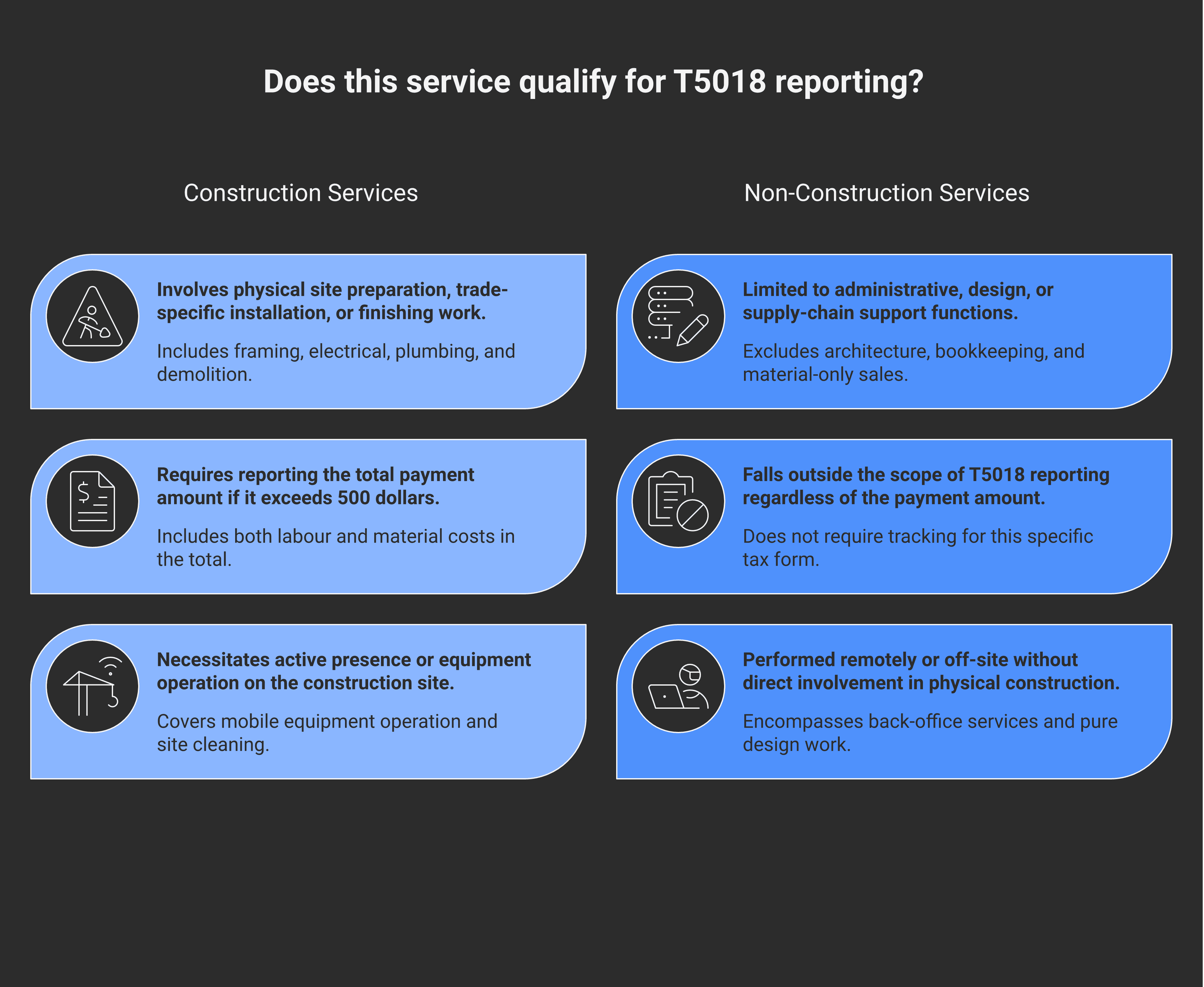

"Construction services" is broader than most contractors think. The CRA's definition follows the work, not the trade:

Site preparation and excavation — yes

Framing, drywall, electrical, plumbing, HVAC, roofing — yes

Finishing trades (flooring, painting, cabinetry) — yes

Demolition — yes

Landscaping when it's part of a construction project — yes

Mobile equipment operation on a construction site (boom trucks, lifts) — yes

Cleaning a finished unit before handover — yes

Pure design work without on-site construction — generally no

If you're not sure whether a sub's work counts, the safer default is to issue the slip. Over-reporting doesn't trigger penalties; under-reporting does.

The $500 threshold

The threshold is $500 per subcontractor across the reporting period, including GST and HST.

Pay a framing sub $480 in March and $470 in October → total $950 → T5018 required

Pay a one-time hauler $475 to move a load of debris → no T5018 (under $500)

Pay a finishing carpenter $4,200 across six invoices → T5018 required

It's per-sub, not per-invoice. Bookkeeping has to track each subcontractor's cumulative payments through the year so you know in real time whose T5018 you'll owe.

The deadline

The deadline is six months after the end of your reporting period. You elect once between calendar year and fiscal year, and that election sticks until you file Form T1135 (no, that's a different form — you stay on your chosen reporting period unless you formally change it via CRA contact).

Calendar-year election (most common for sole proprietors and small corporations): year ends December 31 → deadline June 30

Fiscal-year election: pick any year-end (say March 31) → deadline September 30

The reporting period must match the period of payments. If you pick calendar year, every payment between January 1 and December 31 goes on that year's slips, due June 30 of the next year.

If your business stops operating mid-year, you have to file within 30 days of ceasing operations — not the standard six months.

Filing format — online from 6 slips up

Effective the 2025 tax year, the threshold for mandatory online filing dropped from 50 slips to 6 slips. If you have 6 or more T5018s to file for a reporting period, you must file electronically through CRA's My Business Account or via approved tax software. Paper filing is still allowed for 5 or fewer slips, but most contractors with bookkeeping software file electronically regardless. (Modern Axis covers the CRA paperless transition in more detail.)

The XML schema for the T5018 e-file is published; QuickBooks, Sage, and most contractor-specific accounting platforms generate it directly from the subcontractor payment register. (Authorizing your bookkeeper as a CRA representative is the first step if you want them to file on your behalf.)

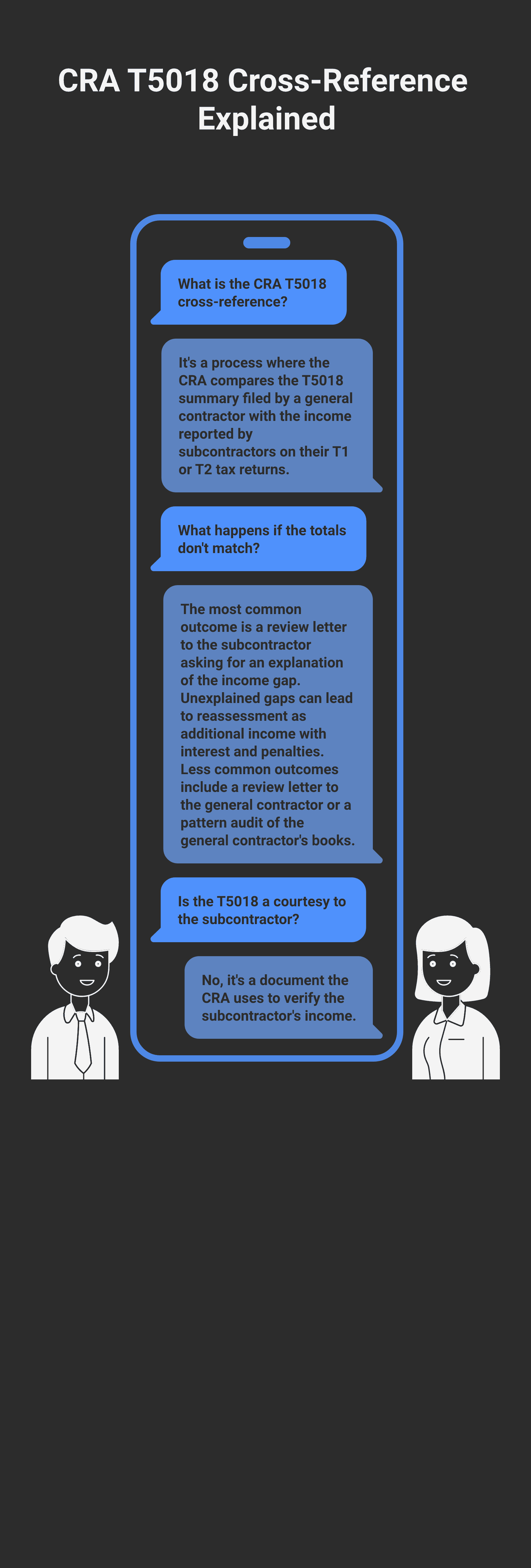

The CRA cross-reference — and what happens when totals don't match

This is where the T5018 trap actually closes.

The CRA receives your T5018 summary listing every sub you paid and the total. The CRA also receives each sub's T1 or T2 return reporting their income. The system automatically cross-references the totals. If you reported paying Sub X $42,000 and Sub X reported income of $28,000 on their T1, that mismatch is flagged.

Three outcomes flow from a mismatch:

CRA review letter to the sub — most common. The sub gets asked to explain the gap. If they can't, the missing $14,000 gets reassessed as income with interest and possibly penalties.

CRA review letter to the general — less common but happens. Did you really pay $42K? Show the cheques and the work order.

Pattern audit — if multiple subs report less than what their T5018s show, the CRA may audit the general contractor's books to verify the construction-services character of the payments.

The takeaway: filing the T5018 isn't a courtesy to the sub. It's the document the CRA uses to verify the sub's income. Every general contractor's accuracy on this slip is what protects (or burns) their subcontractors at tax time.

What to do if you've missed years

Most contractors who realize they should have been filing T5018s for the last 3-5 years come to that realization right after a CRA review letter lands. The right move at that point is not to quietly start filing this year and hope the prior years go unnoticed.

The clean path is the Voluntary Disclosures Program (VDP) — file the missing slips voluntarily, before the CRA contacts you about them, and you can get penalty relief and partial interest relief. (Modern Axis covers the VDP application process in detail.) The VDP requires that:

The disclosure is voluntary (you came to CRA first)

The disclosure is complete (all missing slips, all years)

A penalty would otherwise apply

The information is at least one year past due

If you missed last year only and you're a few months late, file now and pay the late penalty — VDP doesn't help with the current year. If you missed three years across multiple subs, the VDP route is almost always the right answer. (Bookkeeping basics on year-end records covers what documentation you need to reconstruct prior-year subcontractor payments.)

When the T5018 work lands on Contractor Tax Hub

Contractor Tax Hub handles the T5018 prep, the cross-reference against your QuickBooks subcontractor payment register, and the CRA e-file as part of every monthly bookkeeping engagement. If you've been doing your own books and the T5018 list got away from you, the Starter package ($325/month) includes catch-up filing for the current year; prior-year VDP work is a separate engagement. Talk to us before the June 30 deadline (or your fiscal-year equivalent) — the cleanup costs less when it's not also a late filing.

Frequently asked questions

What is a T5018 slip?

The T5018 (Statement of Contract Payments) is the CRA information slip Canadian construction businesses file to report payments made to subcontractors. It's the construction industry's equivalent of a T4A for non-employee labour, with stricter scope — it covers only construction services and only businesses where construction is more than 50% of income-earning activity.

Who has to file T5018 slips?

Any Canadian business where more than 50% of income-earning activities is construction, and which paid one or more subcontractors $500 or more for construction services during the reporting period (calendar year or fiscal year, employer's election). Threshold is per-sub, per-period, including GST/HST.

When is the T5018 deadline?

Six months after the end of your reporting period. Calendar-year filers (December 31 year-end) file by June 30 of the following year. Fiscal-year filers file six months after their fiscal year-end. If you cease operations mid-year, file within 30 days of stopping.

What's the penalty for a late T5018?

$25 per day per unfiled slip, with a minimum of $100 and a maximum of $2,500 per slip. Penalties accrue from the day after the deadline. Twenty late slips at 60 days late is $30,000 in late-filing penalty before any other CRA action.

Do I file a T5018 for an incorporated subcontractor?

Yes. Incorporation doesn't change the T5018 obligation. The slip reports payments to the subcontractor (individual or corporation) for construction services. Whether the sub is a sole prop, a partnership, or a CCPC, if you paid them $500+ for construction work in your reporting period, the T5018 follows.

What counts as construction services?

Site preparation, excavation, framing, drywall, electrical, plumbing, HVAC, roofing, finishing trades, demolition, landscaping when part of a construction project, mobile equipment operation on a site, and pre-handover cleaning. Pure design (architecture, engineering) without on-site work is generally out. The CRA's working definition follows the work, not the trade.

Do I file T5018s for materials suppliers?

No. T5018 reports payments for services, not for materials. A lumber yard sells you materials — no T5018. A framing sub charges you for labour and uses some of their own materials in the work — yes T5018, and the slip reports the total payment including the material component.

I missed T5018 filings for the last three years. What now?

The right move is the Voluntary Disclosures Program. File the missing slips for all years voluntarily, before the CRA contacts you, and you can get full penalty relief plus interest relief. Quietly starting to file this year and hoping prior years go unnoticed almost never works — the CRA's cross-reference catches the gap. Talk to Contractor Tax Hub or a CPA before submitting; the VDP application has to be properly structured.

This is a general overview of how the T5018 rule works, not advice for your business. Filing deadlines, reporting categories, and CRA enforcement policies can shift between tax years, and the right answer for your situation depends on facts not covered above. Contractor Tax Hub can help if you'd like a CPA to look at your numbers — but don't rely on a blog post in place of that.