BC Builders Lien Act Holdback: 10%, 45 Days, Cash Flow

The 10% statutory holdback, the 45-day lien filing window, the section 5 holdback account, and how to track holdback receivables on the books.

BC Builders Lien Act holdback — the 10% statutory retention, the 45-day lien window, holdback accounts over $100K, and the bookkeeping subs miss.

You finished the drywall scope two weeks ago. You invoiced $48,000. The GC paid $43,200. The other $4,800 is "holdback." The GC says you'll get it "when substantial completion is certified." That date isn't on your calendar. The 10% you're owed isn't on your bank statement. And the project superintendent stopped returning calls last Friday.

This post covers the BC Builders Lien Act holdback — what the 10% is, who's required to retain it, how long it sits, when it has to be released, and the bookkeeping side most subs don't account for until their cash flow tightens. The 10% isn't optional and it isn't negotiable; the question is whether you're tracking it like a real receivable or treating it like a number that'll show up eventually. (Our WorkSafeBC for subcontractors post covers the related BC-compliance piece every sub on a jobsite is responsible for.)

Key takeaways

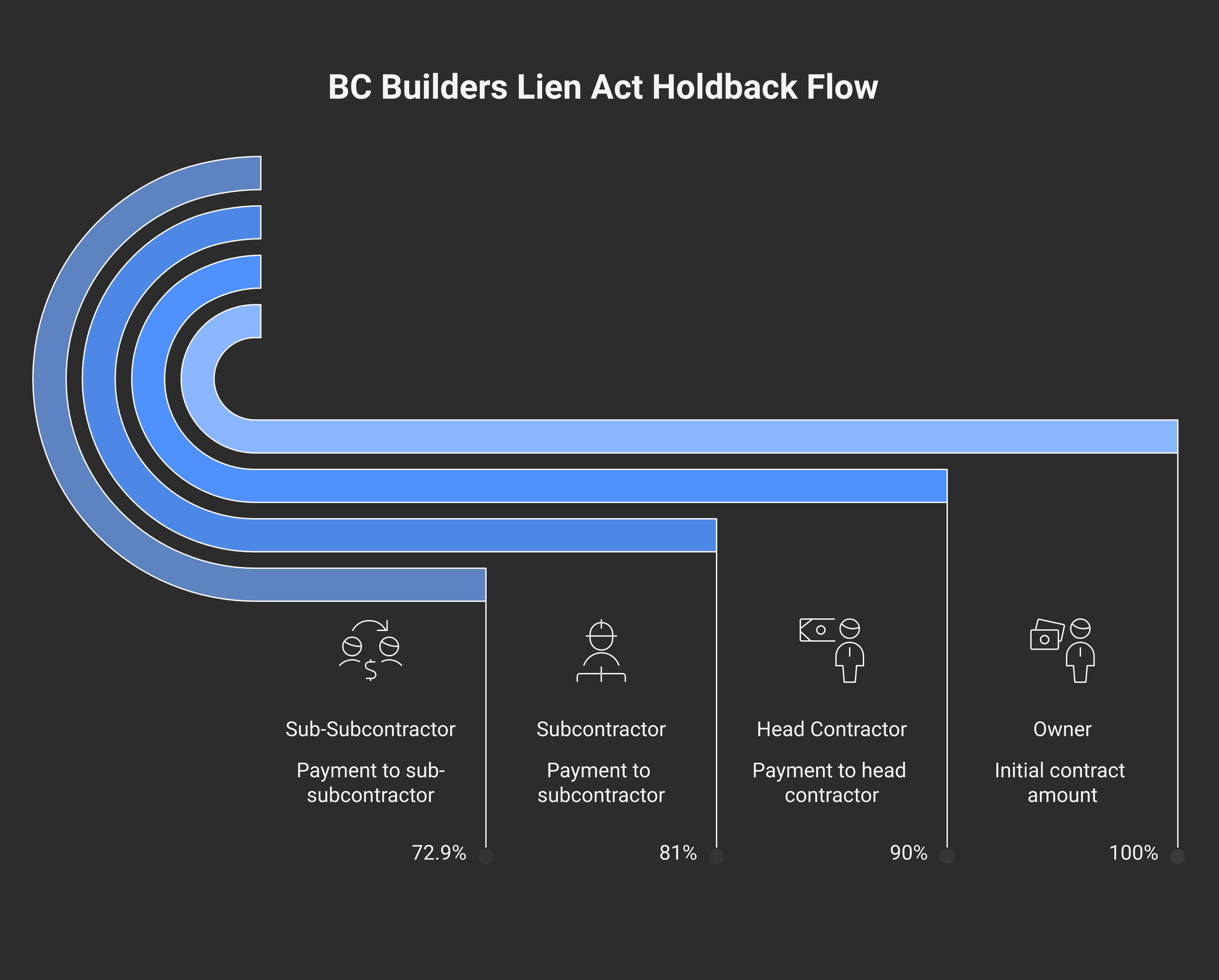

The BC Builders Lien Act requires every payer on a BC construction project to retain a 10% holdback from each payment made downstream — owner from head contractor, head contractor from subs, subs from sub-subs. It's statutory, not contractual.

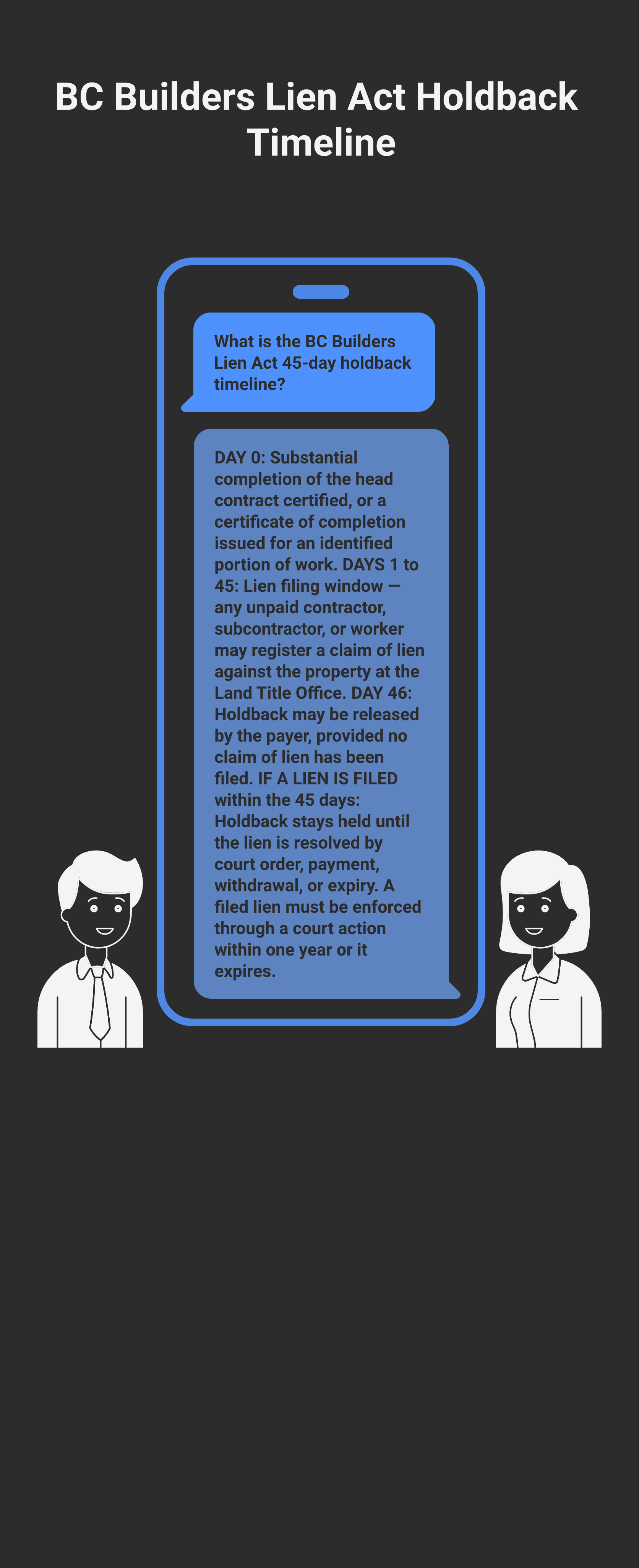

Holdback is released 45 days after the head contract reaches substantial completion (or after the project is abandoned, the contract terminated, or a certificate of completion is issued for an identified portion of work). The 45 days is the lien filing window.

For projects with a contract price over $100,000, the holdback must sit in a separate holdback account at a savings institution, jointly held by the payer and the contractor (section 5 of the Act).

Holdback flows tier-by-tier. Each payer in the chain holds 10% from the tier below. A sub-sub's holdback comes from their immediate payer (the sub), not from the owner.

If you don't get paid within the lien filing window, you can file a claim of lien against the property — a legal charge that forces the owner's attention even if your direct payer has gone silent.

The rule, in one sentence

Under BC Builders Lien Act sections 4 and 5, every person who pays for construction work in BC must hold back 10% of each payment until 45 days after the head contract reaches substantial completion — and on projects over $100,000, that holdback must be parked in a separately maintained holdback account at a savings institution, jointly controlled with the contractor it's owed to. The 10% protects downstream parties' lien rights by guaranteeing a fund the property is liable for, regardless of what happens between tiers above.

The fight is rarely over whether the 10% is owed; it's over when the release clock starts and who counts as substantially complete.

How the holdback flows

The Act doesn't centralise holdback at the owner. It flows tier-by-tier:

Owner ↔ head contractor. The owner retains 10% from each progress payment to the head contractor.

Head contractor ↔ each subcontractor. The head contractor retains 10% from each sub's approved invoice.

Subcontractor ↔ sub-subs and labour-only crews. The sub retains 10% from each tier below.

Three operational consequences:

You get holdback released from your direct payer, not from the owner. If the head contractor goes insolvent before releasing your 10%, your claim is against them — but the lien you can file is against the property, which is what makes the system work.

The 10% is not "the GC's money on hold." Under section 5 of the Act, on projects over $100,000 the GC has to actually park the holdback in a separate joint holdback account at a savings institution. If the GC commingled it with operating cash, that's a section 5 breach.

A late-tier sub waits the longest. Your holdback release clock runs from substantial completion of the head contract, not your scope's completion. The drywall sub who finished in May on a project that doesn't substantially complete until December waits seven months for the 10%.

The 45-day clock

"Substantial completion" of the head contract is the trigger. Under section 8 of the Act, the head contract is substantially complete when the work is ready for use or being used for its intended purpose, and the work to complete the contract can reasonably be done at a cost of 3% of the first $500,000 of contract price + 2% of the next $500,000 + 1% of the remainder.

From the date substantial completion is certified:

Days 1-45: The lien filing window. Any unpaid contractor, subcontractor, or worker may register a claim of lien against the property at the Land Title Office.

Day 46: Holdback may be released by each payer, provided no lien has been filed against that portion of the project.

If a lien is filed within the 45 days: The holdback stays held until the lien is resolved — paid out, withdrawn, court-ordered, or expired (a filed lien must be enforced through a court action within one year, or it expires).

A certificate of completion can be issued for a specific subcontract under section 7, which starts a separate 45-day clock for that scope. Useful for subs whose work finishes long before the head contract substantially completes — but the issuance requires the payment certifier's sign-off, which on many projects means the GC, which means the GC has to cooperate.

The holdback account (projects over $100,000)

Under section 5, on a construction contract where the contract price exceeds $100,000, the holdback must sit in a separately maintained holdback account at a savings institution, jointly held by the payer and the contractor it's owed to. The account requirements:

Separate from operating accounts

Joint signing authority — payer and contractor (or their delegates)

Interest accrues to the contractor whose holdback it is

Withdrawals only on the release conditions in the Act

In practice on small-to-mid BC residential and light-commercial projects, section 5 is often honoured in the breach — many GCs commingle holdback with operating cash. That's a statutory violation. If you're the sub and the GC goes under, the unsegregated holdback is a general unsecured claim against the bankrupt's estate. The segregated holdback account is one of the few pieces of bankruptcy-resistant protection in the system, which is why it exists in the Act.

For incorporated trades managing meaningful holdback receivables, set up dedicated accounts on the books — receivable-holdback as a separate balance, distinct from regular AR. (Modern Books's cash vs accrual primer explains why this distinction matters for revenue recognition.) The 10% you're owed isn't ordinary AR; it isn't due until 45 days after substantial completion, and it carries a different collection profile.

Bookkeeping the holdback right

Three pieces of clean treatment:

1. Track holdback as a separate receivable account

In your accounting system, set up a sub-account under Accounts Receivable: AR — Holdback Retainage. Every invoice that triggers a holdback gets two pieces:

90% to regular AR (gets paid in the current cycle)

10% to AR — Holdback Retainage (sits until release)

This keeps your aging report honest. Holdback isn't 30 days past due — it isn't due. Treating it as ordinary AR makes the report look worse than reality and makes managing real overdue invoices harder. (When you're the head contractor paying subs, holdback also folds into T5018 reporting — the slip reports payments made, including holdback releases when they happen.) (Modern Axis CPA's tax planning service covers the broader cash-flow discipline incorporated trades use to manage holdback receivables alongside instalment obligations.)

2. Recognise revenue when earned, not when paid

If you're on accrual basis (which most incorporated trades are, by CRA default), the full $48,000 in the example above is revenue when the drywall scope is invoiced — regardless of when the $4,800 holdback releases. Tax follows the accrual: the corporation owes tax on the full $48,000 in the year of invoice, not the year of holdback release.

This is the cash-flow gotcha: you owe the tax this year on income you haven't fully collected. Plan accordingly — the corporation needs the cash to fund the tax instalment on holdback income that won't arrive until next year.

3. Reconcile holdback at year-end

Every year-end, run a holdback aging report. For each open holdback receivable:

Project name

Original invoice date

Substantial completion expected

Status (held / released / liened)

Days outstanding

This catches the holdback you forgot to collect — the project that substantially completed nine months ago where the GC never released and you never followed up. The trades that lose the most money to lien-act dynamics are the ones not running this report.

What if you don't get paid?

You did your work. You invoiced. 45 days passed. The holdback didn't release.

Two paths, in order of escalation:

Demand letter. A formal written demand for release, citing section 8 of the Builders Lien Act and the substantial completion date. Many disputes resolve here — the GC was disorganised, not refusing.

Claim of lien. Within the 45-day window (or before it closes if you can move fast), register a claim of lien against the property at the Land Title Office. The lien attaches to the title, which makes the property hard to sell, refinance, or close out — which makes the owner pressure the head contractor, which is often what unfreezes the holdback.

A claim of lien must be filed within 45 days of the work ending (or the certificate of completion being issued for your scope, or substantial completion of the head contract — whichever applies). After 45 days, lien rights expire. After that, you're an unsecured creditor.

The lien must then be enforced through a court action within one year of filing, or it expires.

When holdback discipline lands on Contractor Tax Hub

Contractor Tax Hub sets up holdback receivable tracking, project-by-project holdback aging, and revenue-recognition treatment as part of every monthly bookkeeping engagement for incorporated trades. If you're a sub managing holdback across multiple GCs, or running multi-tier holdback as a head contractor on small residential builds, the Growth or Premium packages carry the project-accounting setup. For trades-corps where holdback timing affects instalment planning, the broader engagement coordinates with the deferred-tax piece.

Frequently asked questions

What is the BC Builders Lien Act holdback?

A statutory 10% retention from every payment on a BC construction project, required under sections 4 and 5 of the Builders Lien Act. Each payer in the construction chain holds back 10% from the tier below. The retention protects downstream parties' lien rights by ensuring a fund the property is liable for if upstream parties fail to pay.

How long is holdback held?

45 days from the date the head contract reaches substantial completion (or the date a certificate of completion is issued for an identified portion of work, or the date the contract is terminated or abandoned). After day 45, the payer may release the holdback provided no claim of lien has been filed against the project within the window.

What is a holdback account, and when is it required?

On any construction contract with a price over $100,000, section 5 of the Act requires the holdback to sit in a separately maintained holdback account at a savings institution, jointly held by the payer and the contractor. Separate from operating cash, joint signing authority, interest to the contractor. Many small projects honour this in the breach — but it's the law, and it's the strongest protection subs have in a GC bankruptcy.

What is "substantial completion" under the Act?

Substantial completion is defined in section 8: the work is ready for or being used for its intended purpose, and the cost to complete remaining work is no more than 3% of the first $500,000 of contract price, 2% of the next $500,000, and 1% of any remainder. The certifier (typically the GC or the architect) issues a written certificate of substantial completion, which starts the 45-day clock.

How do I track holdback in my books?

Set up AR — Holdback Retainage as a separate sub-account under Accounts Receivable. Every invoice that triggers holdback gets split 90% to regular AR, 10% to the holdback sub-account. Run a holdback aging report at every year-end to catch projects where the holdback should have released but didn't. Treat accrual-basis revenue recognition as the default: full invoice is income in the year of invoice, even though the cash arrives later.

Do I pay tax on holdback before I receive it?

If you're on the accrual basis (most incorporated trades, by CRA default), yes — the full invoice is taxable in the year of invoice, including the 10% you haven't collected yet. Sole props on the cash basis recognise revenue when received. The accrual gotcha is the tax cash flow: the corporation owes tax this year on income that lands next year, and instalments have to account for it.

What happens if I don't get paid the holdback?

Two paths. First, a written demand citing section 8 of the Act and the substantial completion date. Most release disputes resolve here. Second, register a claim of lien against the property at the Land Title Office within 45 days of the work ending or the substantial completion date. The lien attaches to title and creates pressure to release. After 45 days, lien rights expire.

Does the owner ever pay me directly?

Only in very specific circumstances. The Act's default is that each payer pays the tier directly below. If the head contractor is insolvent and the owner still holds the head contract's holdback, the Act allows the owner to pay claimants directly out of that holdback in some cases — but the standard path is through the GC. The lien is what creates a direct claim against the property when the chain above breaks.

This is a general overview of how the BC Builders Lien Act works in BC, not advice for your specific project. Substantial completion certificates, holdback release timing, lien deadlines, and the section 5 account requirements all turn on facts not covered above. Contractor Tax Hub can set up your holdback receivable tracking and revenue recognition — but consult a BC construction lawyer for any actual lien filing or holdback dispute.